ASX News LIVE | ASX to Rise; Collins Foods Profits Soar, Paladin Energy Flags Big Move

Market close update

The ASX 200 had a strong session, gaining 1.36% to 7,838.8. All sectors finished up, with Energy stocks the standout gainers today amidst rising oil prices.

Crude oil gained on expectations of stronger demand in the US summer, with Brent hitting a two-month high at US$86.23 per barrel.

The energy sector closed, gaining +2.23%, followed by mining, which finished up +1.83%.

Woodside Energy gained +3.89%, closing slightly above $28 per share, while Santos finished up +2% at $7.65 per share.

While in mining among the mega caps, BHP gained +2% at $43.28, while Fortescue gained 1.5% at $21.58.

Finally, Rio Tinto nearly touched 2% at $121.28 per share, while James Hardie jumped 5% to close at $49.81 per share.

The Big Four banks also had a great showing in the session, with Commonwealth touching an all-time high and gaining 1.13%.

Westpac was up +0.92%, NAB gained +1.78%, and ANZ at the rear gained +0.52% for the session.

Standout performances on the ASX were seen by Collins Food (KFC owners) who reported a 500% gain in statutory NPAT and saw its stock rise +7.62% to $10.03.

Spartan Resources topped the gainers, up nearly 11% to $0.91, followed by Novonix, who added +9.49% to its stock to close at $0.75.

Overnight traders will be keeping a close eye on Japan’s central bank for signs of intervention as the yen continues to slide against its major trading partners.

Consumer sentiment inches up, but still very low

The Westpac–Melbourne Institute Consumer Sentiment Index has seen a slight improvement in June, rising 1.7% to 83.6 from May’s 82.2.

However, this modest gain does little to lift the overall mood, which remains decidedly gloomy.

Senior Westpac economist gave us some context today:

“With the index at 83.6, we’re still far below the ‘neutral’ 100-point mark. Pessimists continue to outnumber optimists by a significant margin – nearly 20 percentage points.”

This mixed economic picture is reflected in consumer expectations, with the survey revealing that 50% of respondents anticipate higher mortgage rates in the coming year.

This small uptick in sentiment, while welcome, is still a drop in the bucket when we look at the persistent economic anxieties facing Australian consumers amid uncertain financial conditions.

Yen’s Plunge Puts Japanese Authorities on Intervention Watch

The Japanese yen’s recent sharp decline has put currency traders on high alert for potential intervention by Japanese authorities to stabilize their weakening currency.

Yesterday, the US dollar surged to 159.94 yen, approaching the 34-year low of 160.245 seen in late April.

That previous dip prompted the Bank of Japan (BOJ) to inject approximately 10 trillion yen ($9.4 billion) to bolster the currency’s value.

The yen’s renewed weakness follows the BOJ’s recent decision to postpone reducing its bond-buying stimulus until its July policy meeting. This year alone, the yen has depreciated by 12% against the US dollar.

The Japanese currency’s decline isn’t limited to its performance against the US dollar. It has also weakened significantly against other major currencies, including the Australian dollar. The yen hit a 17-year low against the Australian dollar on yesterday, marking a more than 10% decline.

This persistent weakness across multiple currency pairs will likely push Japanese monetary authorities to stabilize the yen’s value.

An hour ago, Japanese officials said they would ‘respond appropriately to the excessive volatility’.

Where to find the next major M&A win for your portfolio

As we’ve seen from big moves like BHP’s $64 billion attempt on Anglo American and Paladin Energy’s announcement today— merger and acquisition season is upon us.

This means big miners whose purse strings have remained tight while things have been tough are now out in the world hunting for the next small-cap explorers to corner the market.

If you think BHP will give up after the Anglo attempt, think again; they will no doubt be looking for the next big buy.

Owning one of these small explorers when the buyouts come has resulted in life-changing gains in the past.

For example, at the end of last year, the small-cap lithium miner Azure Minerals rose around 1,500% as the bidding wars broke out for its assets.

Source: Market Index

Resident geologist and M&A veteran James Cooper has seen this before.

Not only was he involved in two prior M&As while in the industry, but he also has something many mining executives lack—deep knowledge of the orebodies and geology of the mines.

With that knowledge, he’s scoured mining reports and sampling to find what he thinks are the next big targets for Mega-cap miners.

If you want to see what he thinks are the next hard targets for M&A, then CLICK HERE for his latest video.

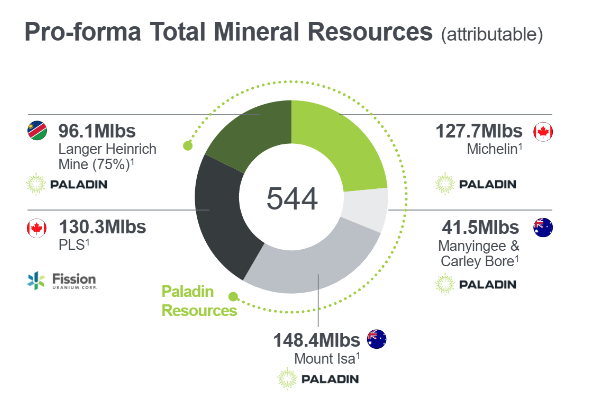

Paladin Shares Drop on Proposed Investment into Canada

Uranium explorer and producer Paladin Energy [ASX:PDN] is down by -7.25% in trading today as the company announces its next big move.

In an investor presentation you can see here the company outlined its big push to create a $5.26 billion uranium giant.

The broad strokes of the plan are to acquire Canadian-listed Fission Uranium and bring its slated Canadian mine into production by 2029.

Paladin, whose Namibian flagship project is far away from its markets, has also proposed creating a massive Canadian hub with its other tenements to serve North American power needs.

Here is what their Total Mineral Resources would look like if the deal is done:

Source: Paladin

The proposal is still in its early days so the stock is likely to see some volatility from here as shareholders and markets react to the potential move.

Midday market update

It’s a green day for the market, with the ASX 200 up by nearly 1% around midday, trading at 7,808.6.

All sectors have gained this morning, with Energy stocks leading the charge, up 1.82% after oil prices began recovering from the weekend’s losses.

Market-cap major Woodside Energy is up by +3%, trading at $27.78 per share, while Santos gained +1.47% to $7.61 per share.

The Big Four banks are all up around 1% today with NAB ahead of the pack, gaining 2% in trading this morning.

In stand-out individual stock performances today, gold exploration company Spartan Resources is up by +8.5%, while last Friday’s massive gainer Encounter Resources is down by -5.65% in trading today.

Qantas Snaps Up Second Hand Planes for QantasLink

Qantas [ASX:QAN] has announced the acquisition of 14 pre-owned De Havilland Dash 8-400 aircraft to bolster its QantasLink regional fleet.

The move aims to gradually replace the airline’s existing 19 smaller Q200 and Q300 turboprop planes.

CEO Vanessa Hudson touted the benefits today, saying:

“By consolidating our turboprops into a single fleet type, we’ll be able to further improve our reliability and provide a better recovery for our customers during disruptions as well as reducing complexity and cost for our operation”.

“These additional Q400s allow us to provide certainty to the regions over the next decade while we work with aircraft manufacturers and other suppliers on electric or battery-powered aircraft that are the right size and range for our network.”

The expansion will increase QantasLink’s total Dash 8-400 fleet to 45 aircraft, serving over 50 regional Australian destinations.

The financial impact of this fleet expansion will be spread across the 2025 and 2026 fiscal years, with the majority of the investment occurring in FY25.

Qantas said that this purchase falls within its current capital expenditure guidance of $3.7-3.9 billion.

Collins Foods net profit jumps 502%

Fast food and KFC operator Collins Foods [ASX:CKF] is today’s market darling after the company announced an incredible 502% statutory NPAT jump for FY24 to $76.7 million.

The company reported record revenue of $1.5 billion, up 10.4 per cent across all business units while reducing debt and increasing cash flow.

Net debt fell -46.7 million to $165.5 million, while Net operating cash flow rose $30.2 million to a total of $165.5 million.

CKF also lifted total dividends by one full cent to 28¢ and said the brand remained ‘growth focused’.

At first glance, you might assume that much of the success of KFC and its other brands like Taco Bell (albeit much less so) could be attributed to recessionary times.

You’d think, ‘oh times are tough so more people are eating at fast foods rather than fancy restaurants.’

However, some studies have come to light that disprove this common assumption.

This study by the US Department of Agriculture showed that numbers remained fairly constant through the last major recession and that time and employment were bigger factors than anything.

So, Collins Foods is just doing well on its own merits.

Morning market update

Good morning. Charlie here,

The ASX 200 opened up +0.76% this morning to 7,792.4 as the market begins to shift into value and cyclicals.

On Wall Street, it was another mixed session as market giant Nvidia moved into correction territory, shedding -6.7% on its third straight negative session after briefly touching the world’s most valuable company.

With oil prices up overnight, energy stocks could be worth watching today after some selloffs and demand concerns yesterday were eventually overcome on the S&P 500 as shipping concerns and longer-term demand expectations pushed crude prices higher.

Wall Street: S&P 500 -0.31%, Dow +0.67%, Nasdaq -1.09%.

Overseas: FTSE +0.53%, STOXX +0.89%, Nikkei +0.54%, SSE -1.17%.

The Aussie dollar +0.18% to US 66.51 cents.

US 10-year bond yields -3bps to 4.23%.

Australian 10-year bond -1bps to 4.20%.

Gold +0.45% to US$2,329.66, Silver +0.50% to US$29.53.

Bitcoin -2.04% to US$62,990, Ethereum -2.5% to US$3,418.

Oil Brent +1.03% to US$86.12, WTI Crude +1.26% to US$81.71.

Iron ore -2.4% to US$102.60 a tonne.

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988