ASX News LIVE | ASX to Rise as Wall St Gains on Inflation Report; July Jobs Data Ahead

Market close update

Australian shares edged 0.2% higher today on the ASX 200 amid a slew of corporate profit reports from some of the country’s biggest companies.

July’s job data was also big news today, showing that Australia’s jobless rate rose 0.1% to 4.2% in July, although the economy still added 58,200 jobs thanks to the impact of mass immigration.

Among the share market movers, Cochlear tumbled -6.7% after its guidance missed expectations, and Origin Energy lost -8.9% as its profit for FY24 made ground, but its guidance for FY25 looked weaker, dragging the utilities sector down to be today’s major underperformed, falling -4.06%.

Elsewhere, the materials sector lost another -1.2%, with BHP (-1.04%), Rio Tinto (-3.58%) and Fortescue (-2.89%) all weaker again, as investors worry about the health of China’s economy.

This was reflected in falling iron ore prices on the Singapore exchange with iron ore futures dropping -2.77% to US$93.0 around a low not seen since 2022.

On Wall Street, the latest US inflation data kept the Federal Reserve on track to cut rates next month, although traders again paired back their bets of a ‘double cut’ to now around 41%, down from high 60’s jut a week ago.

Cochlear drops on earnings report

The medical device company Cochlear [ASX:COH], reported its financial year results today, showing a statutory net profit of $357 million.

The company said it experienced growth across all its business segments, with a notable 9% increase in developed markets, primarily driven by the adults and seniors segment.

However, this profit figure fell short of market expectations, which had projected earnings of $392 million.

Shares are down by -7.5% this afternoon, trading at $312.01 per share. That puts its 12 month return at 27%.

The company’s guidance for the upcoming financial year was also slightly softer than market hopes, forecasting an improved underlying profit ranging between $410 million and $430 million.

Here’s a quick breakdown by CommSec today:

Cochlear $COH forecast underlying profit for the full year of A$410 million to A$430 million. Details below: pic.twitter.com/wgZRPEJuOX

— CommSec (@CommSec) August 14, 2024

Iron ore prices back to 2022 low

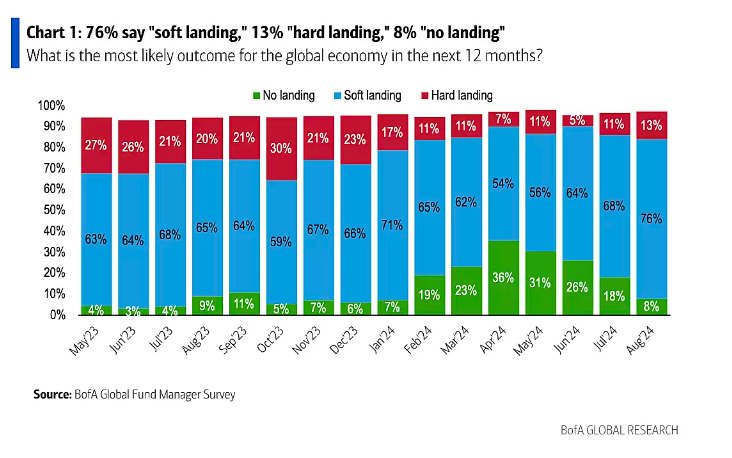

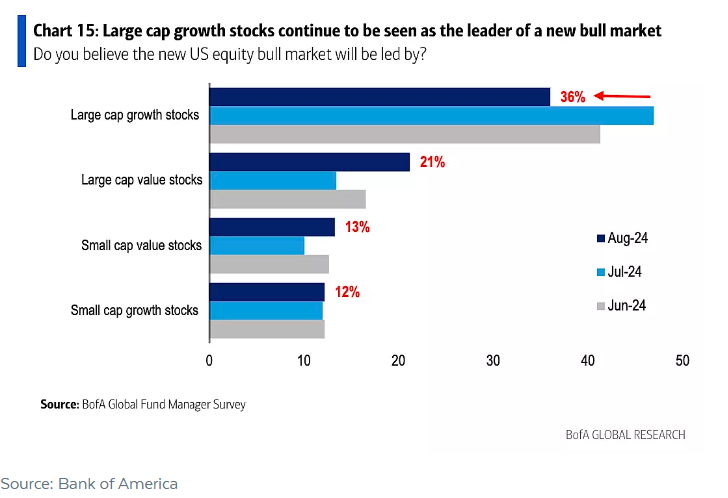

Latest survey from Bank of America fund managers

Now a little over a week since the major market instabilty began, many people have argued about the direction of the market, specifically the US economy and market considering the impact of the Fed’s cuts on global outlooks.

Here is a helpful one from veteran traders in the thick of it.

The Bank of America Global Fund Manager Survey (FMS) offers a window of insight into current market sentiment and positioning.

This monthly survey polls 300 of the bank’s global clients, including institutional investors, mutual funds, and hedge funds.

By capturing the perspectives of major players, the FMS provides a helpful view of how big capital is being allocated and what key market participants are focusing on at present.

So what are fund managers thinking about the chances of a ‘soft landing’?

Source: Bank of America FMS

And what about positioning, what do large fund managers think will lead Wall Street from here:

Source: Bank of America FMS

Midday market update

The ASX 200 is up by +0.38% to 7,880.8 by noon today, with 6 of the 11 sectors in the green.

The latest employment data for Australia helped boost the ASX after its reporting around 11:30 am.

The country’s unemployment rate experienced a slight uptick, rising by 0.1% to reach 4.2%. However, this increase in the jobless rate occurred alongside significant job creation, with the economy adding 58,200 new positions during the month.

Dragging the major sharemarket down so far today is the Utilities sector, falling -4.33% as Origin Energy sheds -10% on its weaker FY25 guidance.

Cochlear was another company that tumbled today despite a fairly solid FY24 performance, with its shares dropping -7.6% to $311.96 per share on softer guidance.

Elsewhere on the major benchmark, we saw the underperformance of major miners as commodity prices continued to struggle to gain amidst weakness from China.

Australia’s Job Market Surges in July, Unemployment Edges Up

Australia’s job market demonstrated unexpected strength in July, with employment numbers significantly exceeding forecasts.

The economy added 58,200 new jobs last month, following June’s increase of 50,200 positions. This surge far surpassed economists’ expectations of 20,000 new jobs.

Despite the impressive job creation, the unemployment rate ticked up to 4.2% from the previous month’s 4.1%, suggesting more people may be entering the job market.

The labour market’s performance is crucial for the Reserve Bank of Australia’s efforts to bring inflation back within its target range, though monthly job reports can be volatile due to seasonal adjustments.

This strong employment data comes against a backdrop of mixed economic signals. While the economy showed minimal growth in the second quarter, there were positive indications in consumer spending.

This data is unlikely to shift the needle on the RBA’s next decision.

Treasury Wines sees statutory profits fall 61%

Penfolds owner Treasury Wines [ASX:TWE] reported a statutory profit after tax of $98.9 million, an over 60% decline from last year.

The drop was attributed to post-materials items loss of $318.1 million ‘relating primarily to cash impairment of good will and commercial brands’.

Despite this, the company saw net sales revenue increase 13% year-over-year to $2.74 billion.

Here’s the overview of their FY24 performance:

Source: Treasury Wines

TWE announced earlier this month it would sell off high-volume, lower-end brands Wolf Blass, Lindeman’s, Yellowglen and Blossom Hill.

CEO Tim Ford also announced a further step in restructuring, with the group to merge its Treasury Premium Brands business with its Treasury Americas premium brands portfolio by mid-2025.

The company announced a final dividend of 19 cents, up from 17 cents last year.

Goodman Group beats guidance

Industrial property and data centre giant Goodman Group [ASX:GMG] topped its full-year earnings guidance today, reporting a 14% increase in operating earnings per security to 107.5 cents.

This topped the company’s May guidance of 13% EPS growth, which was already an upward revision from the initial 9%growth forecast at the start of FY24.

The company said its strong performance was thanks to robust global demand for warehouse space near urban centres.

Goodman’s operating profit was $2.049 billion, a 15% increase from the previous fiscal year.

However, despite the positive operational results, Goodman Group recorded a statutory loss of $98.9 million.

This loss was due to a 3% decrease in the total portfolio value, which fell to $78.7 billion following revaluation declines of $5.1 billion across the group and its partnerships.

The company maintained its full-year distribution at 30 cents per security.

Here is an overview from the report:

Source: Goodman Group

Notably, data centres now represent a significant chunk of Goodman’s global project pipeline, accounting for 40% of the $13 billion total.

Looking ahead, CEO Greg Goodman expressed confidence in the company’s position ‘despite global market uncertainty’ for FY25, citing a strong development workbook and solid capital position.

The company projects FY25 operating EPS to reach 117.2 cents per security, a 9% increase from FY24.

Origin Energy Profits Jump

Origin Energy [ASX:ORG] has reported a ‘significant uplift‘ in its financial performance for the full fiscal year ending 30 June 2024.

Net profit jumped by 32%, reaching $1.397 billion, up from $1.055 billion in the previous year.

The company’s core profit saw an even more substantial rise, surging almost 60% due to improved earnings in both its energy markets and gas supply divisions. Revenue also saw a modest increase of 2%, totalling $16.138 billion.

The company’s underlying profit for the year reached $1.183 billion, a significant increase from $747 million in the prior period.

Despite the positive results, CEO Frank Calabria cautioned that the energy markets business is expected to face softer profits in the coming year, a sentiment echoed by competitor AGL Energy recently.

Calabria pointed to several factors for future softness, including the repricing of electricity tariffs to reflect lower wholesale costs, retail margins, and higher coal costs.

However, looking further ahead, he remained positive, saying:

‘Over the medium term, we believe Origin’s leading customer position, diverse portfolio of energy assets, and growing renewables and storage pipeline, combined with access to global growth through Octopus Energy, positions the company advantageously as the energy transition progresses. Origin is in a strong position to deliver value for our customers, communities and shareholders.’

Origin increased its final dividend to 27.5 cents, up from 20 cents the previous year.

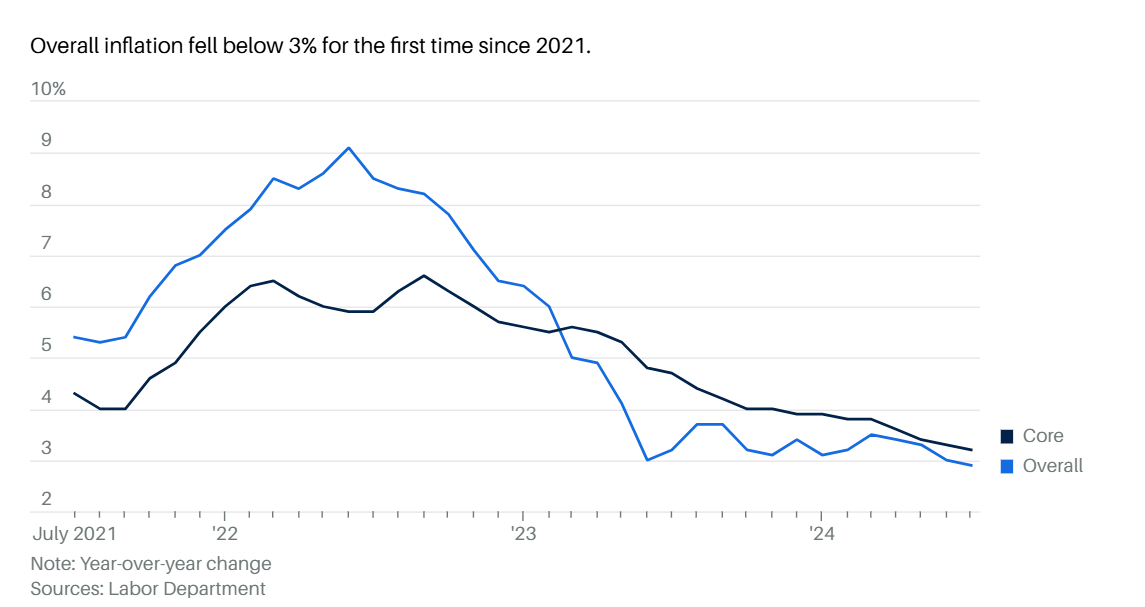

US CPI print shows steady drop

Overall inflation in the US fell below 3% for the first time since 2021, according to the latest CPI report.

The Bureau of Labor Statistics reported inflation of 2.9%, slightly below the expected 3% increase.

Monthly, that was a 0.2% increase, which was in line with expectations, while core YoY showed a 3.2% increase, which also had an in-line monthly increase of 0.2%.

The slow and steady inflation drop meant traders cut their bets of a half-point cut in September (above the usual 0.25bps cut).

Traders are now pricing in a 41.5% chance of a double cut in the September FOMC meeting, that’s a steady decrease from 53% on Tuesday and 69% just a week ago.

Source: Barrons

Morning Market Update

Good morning. Charlie here, back on ASX live after a bout of illness.

The Australian share market is set to rise today as several major ASX companies report earnings.

Today, we have Goodman Group, Origin Energy, Telstra, and Treasury Wines reporting, so stay tuned for those.

Beyond the earnings on the Australian share market, we have the July job report at 11:30 am AEST, so stay tuned for that.

ASX 200 Futures are up 0.04%, pointing to gains following Wall Street as a steady CPI report from the US has many believing the Fed is on track for cuts next month.

Most major tracked commodities fell overnight, with sharp falls in gold, iron ore, and oil, which could pressure local producers.

A US government report on crude oil sent prices down -1.26% after it noted a rapid build-up of US crude stockpiles.

Iron ore saw a sharp -2.4% drop before recovering slightly after a major Chinese steelmaker, Baowu, warned investors about a ‘long and harsh winter‘ ahead for the steel industry.

| Name | Value | % Chg | |

|---|---|---|---|

| Major Indices | |||

| S&P 500 | 5,455 | +0.38% |

| Dow Jones | 40,008 | +0.61% |

| NASDAQ Comp | 17,192 | +0.03% |

| Russell 2000 | 2,084 | -0.52% |

| Country Indices | |||

| UK | 8,281 | +0.56% |

| Germany | 17,885 | +0.41% |

| Euro | 4,727 | +0.70% |

| Japan | 36,442 | +0.58% |

| Hong Kong | 17,113 | -0.35% |

| Name | Value | % Chg | |

|---|---|---|---|

| Commodities (USD) | |||

| Gold | 2,423 | -0.66% | |

| Silver | 27.57 | -0.92% | |

| Iron Ore | 95.60 | -0.05% | |

| Copper | 4.0215 | -0.75% | |

| WTI Oil | 77.36 | -1.26% | |

| Currency | |||

| AUD/USD | 65.97¢ | -0.57% | |

| Cryptocurrency | |||

| Bitcoin (USD) | 58,975 | -2.75% | |

| Ethereum (USD) | 2,668 | -1.77% | |

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988