ASX News LIVE | ASX to Open Flat; Big Earnings Day with BHP and Coles Reporting

Market Close

The share market edged lower today as a flat opening slowly fell throughout the session as investors weighed corporate reports and rising commodity prices.

The ASX 200 fell -0.17% to 8,071.2 with little movement through the day as Energy stocks helped buoy much of the market as tensions in the Middle East once again drove oil prices higher.

8 of the index’s 11 sectors were in the red, led by tech and banks. Energy trimmed gains later in the session but was still the top sector, up by +2.34%.

A sizable chunk of trading activity focused on Woodside, BHP, Coles and Worley after the companies posted results todaay, with Woodside and Worley among the top gainers.

Shares in Woodside jumped 4.17% after reporting a smaller-than-forecast decline in net profit in the six months to June as LNG prices softened. A higher dividend payout and promises to not tinker with dividend policy also saw investors favour the trade today.

Further underpinning the energy sector was a 3% spike in crude oil prices overnight, with Brent climbing above US$81 a barrel on supply concerns after Libya’s government shut down some of its oil fields.

Israeli strikes into Lebanon also stirred concerns of further escalation within the Middle East as ceasefire talks once again hit a roadblock.

Index-heavyweight BHP rose 1.52% after a slightly better-than-expected US$13.7 billion underlying profit.

Supermarket giant Coles advanced 1.9% after reporting stronger full-year net profit in fiscal 2024, taking total dividends to 68 cents fully franked. Global engineering group Worley leapt 3.3% thanks to higher profits in 2024.

Latest Fat Tail Daily Video

Here’s day two of our new Fat Tail Daily video series.

We’ve heard that you want more discussions with editors about market movements and their thoughts — and we’ve listened!

Publisher James ‘Woody’ Woodburn will be sitting down with our Fat Tail Daily editors to discuss the key trends and offer unique insights into market movements.

Expect more of these coming soon. Depending on schedules, we will aim to get at least three out a week, but it could also be more.

If you have any thoughts about the length, format, or any topics you would like discussed, send us an email at support@fattail.com.au with the subject header: ‘Fat Tail Daily Video Feedback’.

Thanks, and enjoy today’s discussion with Diggers and Drillers and Mining Phase One Editor James Cooper.

Midday market update

The Australian sharemarket remains flat around midday, with the ASX 200 down -0.02% to 8,082.8 as the Energy sectors help hold the line as oil prices jumped 3% overnight.

Woodside Energy is up by +4.57%, while Whitehaven Coal has increased nearly 3% in trading so far today. Santos is also up by +2.5%, trading at $7.455 per share.

Materials are also up today, as BHP reports. They saw a slight earnings upside, while other major miners saw a boost thanks to a 4% gain in iron ore futures on the Singapore exchange, breaking the US$100 per tonne.

Only four of the eleven sectors are in the green around midday, with Tech today’s laggard, falling -1.23% so far today.

Major moves on reporting today have been; Coles up by +2.4% after its earnings saw growth in supermarket earnings.

Worley gained +3.6% as it saw profits jump compared to its weaker financial year in FY23.

Johns Lyng Group fell sharply, down by -25.4% after reporting a sizable revenue fall in its reporting today.

Jewellery retailer Lovisa fell nearly 14% despite higher profits as its trading update failed to wow.

Coles rises on earnings report

Supermarket giant Coles [ASX:COL] shares rose by +2.1% in trading this morning after it reported its FY24 results.

The group saw its EBITDA rise by 5% to $3.65 billion, while net profits after tax were up 2.1% to $1.12 billion for the financial year.

The company declared a final dividend of 32 cents per share, bringing its full-year dividend to 68 cents per share.

The standout performance from the results was the growth in eCommerce sales, with sales on its online platform growing by 30.1% in Supermarkets and 9.2% in liquor.

Coles CEO, Leah Weckert said:

‘The financial pressures on households and families have been front of mind for us this year and we have endeavoured to deliver value across our supermarket, liquor and online offerings to help customers balance the household budget. At the same time, we have worked hard to deliver improvements in availability and quality, made significant inroads in addressing loss, accelerated our digital offering, continued to maintain a strong focus on costs and completed the construction of our second ADC and both our CFCs.’

Total group revenues were 5.1% higher, with most of that growth coming from the supermarkets, which saw revenues increase by 6.2%, while liquor grew by only 2.3% in the financial year.

A similar story was seen in earnings, with supermarket earnings up by 14.3%, while liquor fell by -15.3%.

The outsized earnings to sales will likely continue to raise questions for the major retailer as the inquiry into price gouging by Coles and Woolworths continues by the ACCC.

The inquiry is expected to release its interim report in a few days, while the final report is expected around the end of February next year.

Looking ahead to FY25, the company said it has seen positive momentum in the first eight weeks of FY25 in supermarket volumes and revenues. However, liquor continues to drag, with early sales revenue showing a 1.4% decline.

Capex for FY25 is expected to be around $1.2 billion as the company opens eight new stores and invests in its digital offering.

Bullish or bearish on uranium?

Australian uranium producers are back in the spotlight after their huge jump yesterday.

Deep Yellow, Paladin, and Boss Energy all jumped over 10% yesterday after the world’s largest producer, Kazatomprom, released guidance that fell short of market expectations over the weekend.

Is the recent winter for uranium stocks over, or is this a one-time jump?

For many, the underlying story is one of long-term supply deficits, but will the West adopt nuclear or continue on the road to renewables?

As uranium gains support throughout the world, decades of disinterest means chiefly this:

Few new mines likely to be ready when needed.$FCU

📊 @quakes99 pic.twitter.com/bv5qVbgXng

— Paola Rojas 🐝 (@paola_rojas) August 26, 2024

Worley rises on reporting, issues warning

Worley [ASX:WOR], the global engineering group, reported its FY24 results today, showing a significant profit increase.

The company’s annual net profit jumped to $303 million, up 27%, partly due to favourable comparisons with the weaker prior year.

Underlying earnings grew 24% to $751 million, excluding a $58 million writedown. The company’s workforce expanded by 3% to 49,700 employees.

While much of this was positive compared to last year, CEO Chris Ashton did issue some warnings about future prospects. He noted a rise in cancelled and scaled-back energy projects, citing geopolitical shifts and economic factors as causes for delayed client decisions. That resulted in a 2% drop in work backlog.

Despite this, he was positive today, saying:

‘We’re consistently delivering on our strategy as demonstrated by increased earnings, margins and cash flow. Our aggregated revenue represents the highest in Worley’s history, with increases across all regions and each of the three segments of energy, chemicals and resources contributing to this result.’

Worley maintained its total dividend at 50¢ per share, with a final dividend of 25¢.

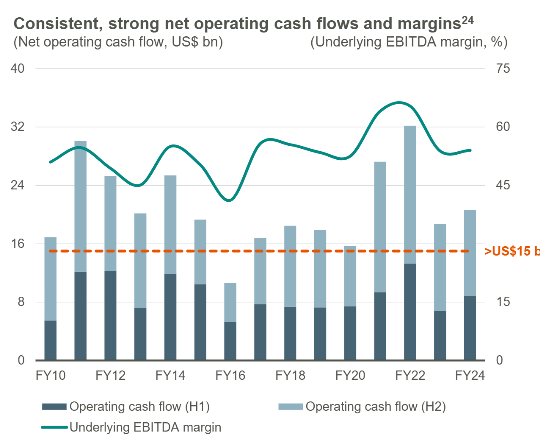

BHP shares rise on earnings

Mining giant BHP reported its FY24 earnings this morning. So far the market reaction has been positive, as the company reported a slightly higher-than-expected underlying earnings of US$13.7 billion, up 2%.

Revenue was also up 3% to US$55.7 billion, thanks to higher realised prices across copper and iron ore and a rise in sales for both. However, attributable profit was down 39% to US$7.9 billion.

Source: BHP

Underlying EBITDA saw a 4% improvement, while underlying margins were flat at 54%. That’s the eighth consecutive year with margins above 50% for BHP.

Operational cash flow increased 11% to US$20.7 billion as the company’s tax bill came down.

The company’s free cash flow was up 111% to US$11.9 billion as the company looks to spend around US$6 billion in acquiring and exploring for more copper projects.

Looking ahead the company said it expects to spend US$10 billion in FY25 and US$11 billion in FY26 in capex and exploration.

The company declared a final dividend of US$0.74 per share will be paid on 3 October, bringing the full-year dividend to US$1.46 per share.

That’s down from last financial year’s US$1.70 dividend as the company holds capital back to look for more acquisition targets as it looks towards a future growth.

Morning Market Update

Good morning. Charlie here.

The ASX 200 opened flat at +0.09% 8,091.4 as markets began the day with more cautious trading, mirroring a mixed day on Wall Street as both the S&P 500 and Nasdaq retreated.

Traders seem to favour big-name blue chips as the Dow Jones closed at record highs thanks to corporate earnings.

For macro signals, we saw US July durable goods orders surprise to the upside, while commodities had a strong session overnight.

Crude oil jumped over 3%, with WTI Crude reaching US$77 per barrel, marking the third consecutive session of gains as supply risks from potential conflict in the Middle East once again took centre stage.

Iron ore Futures on the Singapore exchange reclaimed US$100 per tonne after climbing over 4% in trading overnight.

A positive catalyst for the big earnings report today by BHP, whose early read shows an underlying net profit of US$13.7 billion for FY24. I expect it to be a positive day for the big miner, likely lifting the ASX 200 with it.

Looking ahead this week, we have:

Wednesday: Australia – July CPI indicator, Q2 construction work

US – Nvidia earnings results

Thursday: Australia – Q2 Building capex

Friday: Australia – July retail sales, private sector credit

US – PCE and core inflation

Europe- CPI

| Name | Value | % Chg | |

|---|---|---|---|

| Major Indices | |||

| S&P 500 | 5,616 | -0.32% |

| Dow Jones | 41,240 | +0.16% |

| NASDAQ Comp | 17,725 | -0.85% |

| Russell 2000 | 2,217 | -0.04% |

| Country Indices | |||

| UK | 8,327 | +0.48% |

| Germany | 18,617 | -0.09% |

| Euro | 4,896 | -0.25% |

| Japan | 38,110 | -0.66% |

| Hong Kong | 17,798 | +1.06% |

| Name | Value | % Chg | |

|---|---|---|---|

| Commodities (USD) | |||

| Gold | 2,516 | +0.02% | |

| Silver | 29.9 | -0.05% | |

| Iron Ore | 100.25 | +4.01% | |

| Copper | 4.1964 | -0.11% | |

| WTI Oil | 77.14 | +3.09% | |

| Currency | |||

| AUD/USD | 67.73¢ | -0.22% | |

| Cryptocurrency | |||

| Bitcoin (USD) | 62,937 | -2.11% | |

| Ethereum (USD) | 2,684 | -2.26% | |

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988