ASX News LIVE | ASX to Fall with Wall St as Fed Dispels Hopes of March Cut

Market close update

The ASX 200 closed down 1.20% to 7,588.2 as markets reacted to the Fed’s rebuttal of expectations of an early rate cut in the US.

We also saw some shakiness in US banks throughout the session, which spilled over into our Big Four as US lender New York Community Bank fell over 37% after warning of rising bad debts after cutting its dividend payments.

On the ASX 200 all sectors were down, with the biggest losers Financials (-1.81%) and Real Estate (-1.67%).

We also saw falls in Microsoft (-2.7%) and Alphabet (-7.5%) despite both double beats as certain segments disappointed traders who couldn’t justify the high share prices.

For Microsoft, cloud revenue was up 28% but lower than the hoped 30%, while for Google ad revenues came in a few hundred million shy.

In the FOMC meeting overnight, the US central bank kept rates on hold at 5.25-5.5% and said it ‘needed more confidence before cuts‘.

The FOMC also made notes on:

Needing more data:

‘The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2%.’

Economy looking strong:

‘Recent indicators suggest that economic activity has been expanding at a solid pace,” notably persistent wage inflation, stronger-than-expected Q4 GDP and strong job gains.’

Fed Chair Jerome Powell had his usual post-conference meeting where he made some remarks that pushed back on the market, making some key points on:

Peak rates here:

‘We believe that our policy rate is likely at its peak for this tightening cycle and that if the economy evolves broadly as expected, it will likely be appropriate to begin dialing back policy restraint, at some point this year’

Unlikely to cut in March:

‘Based on the meeting today, I would tell you that I don’t think it’s likely the committee will reach a level of confidence by the time of the March meeting to identify March as the time to do that. But that’s to be seen.’

Trouble brewing in Europe

It seems the ECB’s fears are coming alive with the latest rounds of data from the Eurozone.

The continent recorded a flat quarter of GDP growth, with contractions abound.

🇪🇺 The Euro Area is clearly stagnating, and quite possibly will not be able to start growing without rate cuts by the ECB

➡️ QoQ: 0% real GDP growth, with contractions in Ireland, Germany, Lithuania and a stagnation in France

➡️ YoY vs Q4-22: 0.1% real growth, with contractions… pic.twitter.com/ybEFqkS5oZ

— Nikolay Kolarov, CFA (@libertniko) January 30, 2024

Breakdown of consumer good import prices

The latest data is out on consumer goods import prices, and its pointing to some uncomfortable news.

While the latest CPI data showed price increases are slowing at an ever-increasing speed, the hope of prices actually falling might remain a pipe-dream.

Consumer good import prices show that imported inflation is still a factor that is playing out in the economy.

The Red Sea attacks by Yemen Houthis aren’t helping the situation, as shipping costs remain 150% higher than December prices.

Source: Freightos

Here is the latest data from Economist Alex Joiner and IFM.

All consumer good import category prices rose, particularly cars. These data also underscore an important point that yes inflation is slowing but prices are, on average, not falling and will likely stay materially higher https://t.co/UrsNjIW167 pic.twitter.com/hv7KSSz11I

— Alex Joiner 🇦🇺 (@IFM_Economist) February 1, 2024

Midday market update

The ASX 200 is down by -1.05% at 7,600.2, coming down from its record high after the Fed pushed back expectations of a March rate cut after keeping rates on hold overnight.

The Australian benchmark is now down 0.1% for the year to date, after a strong correction today.

All 11 sectors are down, with Technology the worst hit today, falling -2.08%, while the best performer was Staples, falling -0.54%

Notable stock movements today were seen by Emerald Resources which fell -5.39%, the biggest loser on the ASX 200 at midday.

IGO also fell sharply, down -3.24% after its double negative news yesterday of poor quarterly performance and the mothballing of its Cosmos nickel project in WA.

Tech player Block also fell sharply, down -3.04%. This puts their performance in the past 12 months at -12.65%.

Interestingly, most of the large-cap players in the ASX 200 have held their losses to below 1% so far in trading today, but more are likely to slip later in the session.

December building approvals disappoint as house prices climb

It’s a tale of two cities today. The ABS released December’s building approval numbers, which were down -9.5%. Far away from the expectations of +0.5%.

Source: ABS

The ABS blamed the shortfall on a decline in apartment approvals. As Daniel Rossi, ABS head of construction statistics, said today:

“Approvals for private sector dwellings excluding houses drove the December decline, falling 25.3 per cent. In 2023, there were 59,174 private other dwellings approved, compared to 73,041 in 2022. This reflects a 19 per cent annual fall.”

Meanwhile, house prices are on track to continue to rise across the country as renters and migrants push into the housing market, propelled by high rent cots and folks wanting to move ahead of interest rate cuts expected to propel the market further up.

Data from CoreLogic showed that house prices rose 0.4% nationally in January, up from 0.3% in December. That’s an 8.7% increase for 2023.

It marked the 12th straight month of gains, with the largest seen in Perth (+1.6%), Adelaide (+1.1%) and Brisbane (+1%).

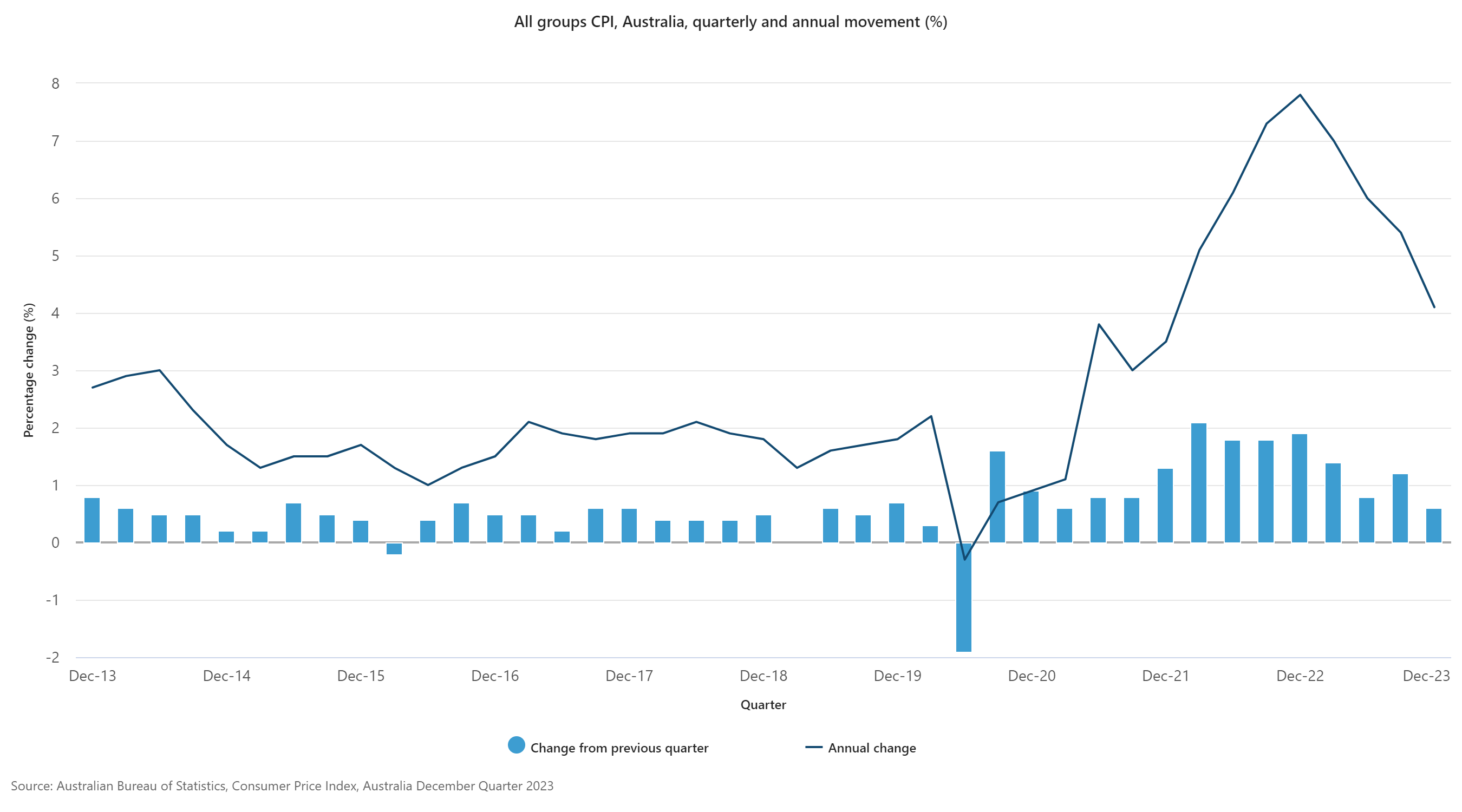

Australian inflation falls faster than expectations

Yesterday’s CPI data came in at +0.6% for the quarter.

That’s 4.1% on an annualised basis, below the expected +0.8% and 4.3% p.a.

The important food and energy categories showed meaningfully slower price increases, while insurance was the big outlier, with prices up 16.2% in the past 12 months.

Source: ABS

With the unexpectedly strong drop in inflation, markets have brought forward their expectations of rate cuts.

Traders are now pricing two 0.25% rate cuts by the end of the year.

The first fully priced in cut is by August 2024, back from the previous September expectation.

The market still expects the RBA to keep rates on hold at next week’s meeting, but signs are hopeful.

Prime Minister said yesterday’s move was ‘encouraging progress’, welcoming the news as the government tries to sell its changes to stage 3 tax cuts.

Morning market update

Good morning. Charlie here

The ASX 200 opened down -0.32% to 7,656.1 as Western markets corrected after a strong runup through January.

The big catalyst for the drop today was the speech by Jerome Powell and the signalling from the Fed that interest rates are likely to be cut later than traders hoped.

The Fed kept US interest rates on hold last night at 5.25–5.5%, saying it saw positive signs of inflation falling in the past 6 months, but it was too early to declare victory on inflation just yet. Jerome Powell’s comments in the conference afterwards summed this up saying:

‘Based on the meeting today, I would tell you that I don’t think it’s likely the committee will reach a level of confidence by the time of the March meeting to identify March as the time to do that. But that’s to be seen.’

A few weeks ago, traders were pricing in an 80% chance of a March cut, but that fell to just under 50% earlier this week. It’s now at just 35% this morning.

Wall Street: Dow -0.82%, Nasdaq -2.23%, S&P 500 -1.61%.

Overseas: FTSE -0.47%, STOXX -0.31%, Nikkei +0.61%, SSE -1.48%

The Aussie dollar fell -0.52% to US 65.66 cents.

US 10-year bond yields fell -12bps to 3.91%.

Australian 10-year bond yields fell -18bps to 3.95%.

Gold rose +0.11% to US$2,038.73. Silver fell -1.01% to US$22.93.

Bitcoin fell -1.63% to US$42,592, while Ethereum fell -3.46% to US$2,284.

Oil Brent fell -1.40% to US$81.71, while WTI Crude fell -2.61% to US$75.79.

Iron ore fell -2.4% to US$129.60 a tonne.

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988