ASX News LIVE | ASX to Fall; Bapcor Receives $1.83b Bid, Beach Energy Flags $400m Hit

Market close update

The ASX 200 closed down by -1.41% to 7,749.1 as investors braced themselves for the US Federal Reserve’s potential pushback against immediate rate cuts during its upcoming policy meeting this week.

Political uncertainty in Europe, stemming from the far right’s substantial advances in the European elections and a surprising poll in France, further dampened market sentiment, reviving concerns about the Euro bloc’s future.

The mining sector and utilities led the decline, with 10 out of 11 sectors in the red. Index heavyweights BHP, Rio Tinto, and Fortescue retreated by 1.8%, 2.2%, and 2.9%, tracking lower iron ore prices.

Gold miners also suffered significant losses after the precious metal experienced its most substantial drop in three years last Friday. The price closed at the end of the session today around US$2,300 per ounce.

The decline was triggered by a strong US jobs report, which diminished hopes for rate cuts, and reports suggesting that China’s central bank was holding off on gold purchases.

West African Resources was the biggest laggard on the index, falling by more than -8.8%, while Ramelius, St Barbara, and Bellevue Gold shed over 5% each.

Investors are cautious ahead of key US consumer price data on Wednesday and the Fed’s rate announcement on Thursday (AEST), where the central bank is expected to maintain rates but revise its quarterly projections to indicate fewer rate cuts than previously forecast.

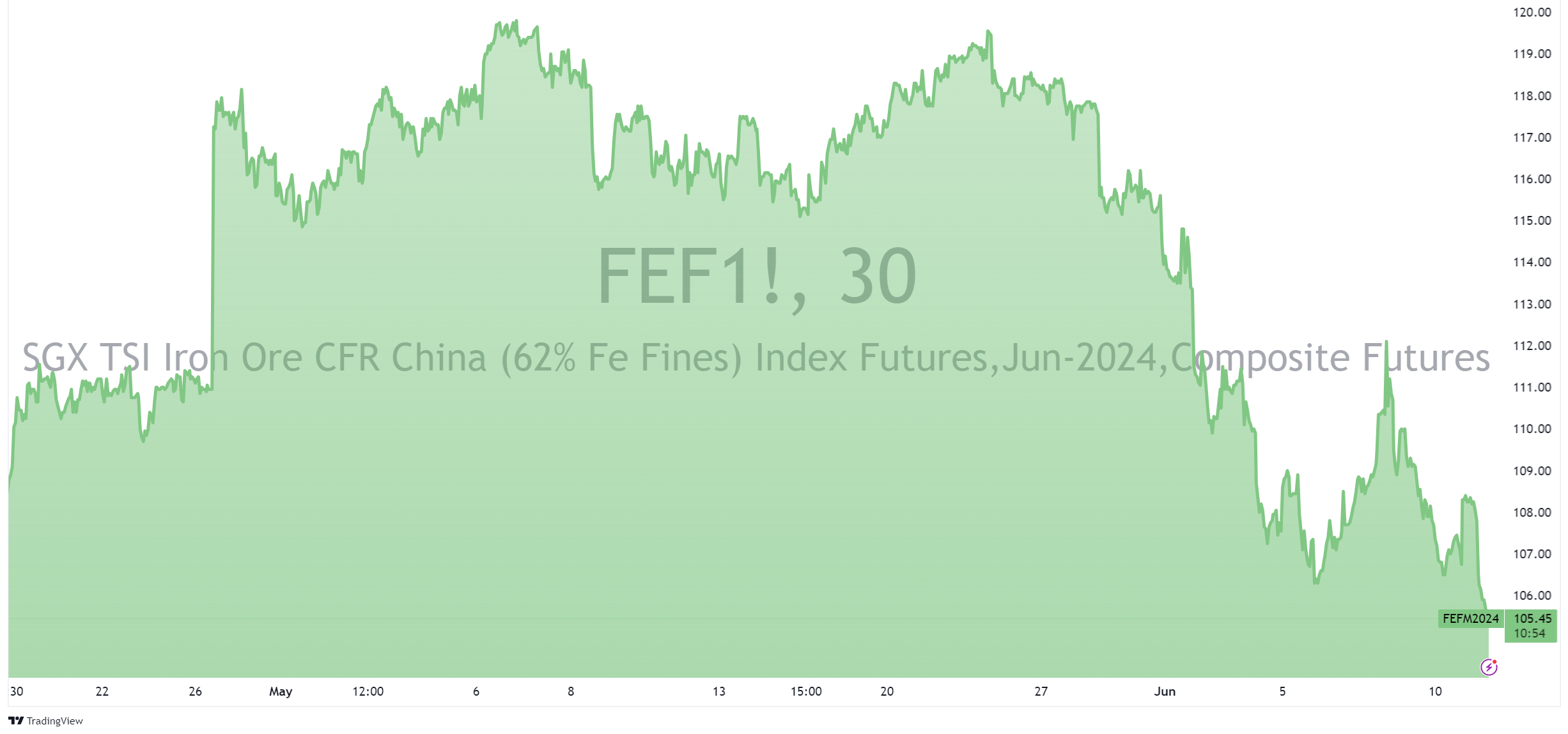

Iron Ore Prices Plunge as China’s Demand Weakens

Iron ore futures have dropped to a two-month low due to weak fundamentals and concerns over China’s demand following the country’s latest carbon emission plan for the steel sector.

The September iron ore contract on the Dalian Commodity Exchange closed 3.69% lower at 810 yuan per metric ton, while the July iron ore on the Singapore Exchange fell 0.9% to $US104.45 a ton.

Source:TradingView -Singapore Exchange Futures

Analysts cite increased supply, weakened demand, and high port-side inventory as factors contributing to the market pressure. China’s state planner recently announced a plan to reduce carbon dioxide emissions in the steel sector by 53 million tons between 2024 and 2025, which could lead to a significant reduction in hot metal output.

There is also growing doubt about the effectiveness of China’s property stimuli in boosting real steel demand. The country’s efforts to convert unsold homes into affordable housing may not significantly help cash-strapped developers due to the program’s limited size and potentially low prices.

New Zealand Abandons Plan to Tax Agricultural Emissions

The New Zealand government has decided to scrap its plan to impose a tax on agricultural emissions, including methane produced by sheep and cattle.

The decision comes as a result of intense pressure from farmers who argued that the scheme would render their businesses unprofitable.

The conservative government has announced the formation of a Pastoral Sector Group, which will include representatives from the agricultural sector. The group’s primary objective will be to explore alternative methods for reducing biogenic methane emissions without resorting to taxation.

New Zealand, a nation of 5 million people, is home to around 10 million cattle and 26 million sheep. Remarkably, nearly half of the country’s total greenhouse gas emissions can be attributed to agriculture, with methane being the primary culprit.

To support the transition towards more sustainable farming practices, the government has pledged NZ$400 million over the next four years.

These funds will be directed to reduce on-farm emissions, providing farmers with alternative solutions to mitigate their environmental impact.

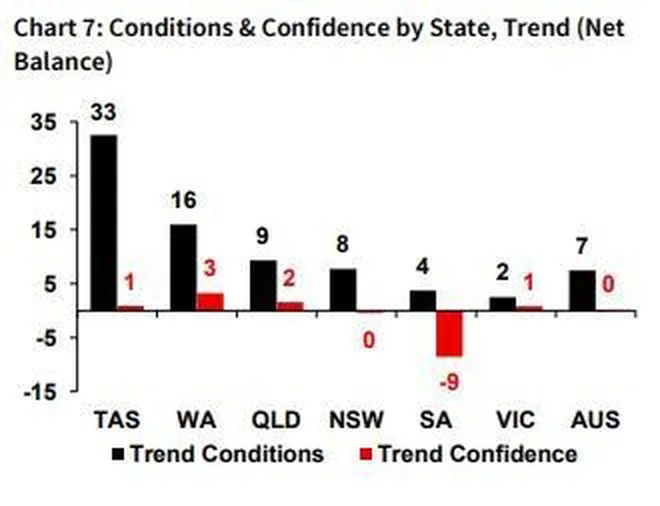

NAB Business Confidence takes a dive in SA

NAB’s latest business confidence survey showed relatively stable (but low) levels of business confidence for the Eastern Australian States.

However, spare a thought for our neighbours, with Tasmania, WA, and SA all experiencing sharp drops in the past month.

According to NAB:

“By state, conditions were little changed in the eastern states but fell sharply in Tas, WA and SA. In trend terms, WA and Tas remain more elevated with most states still at reasonable levels. Trend conditions in Vic remain softest at +2 index points.”

Source: NAB Business Confidence Survey

NAB continued:

“There were falls in conditions across most consumer-facing sectors including retail and recreation and personal services, while forward orders remained negative overall with deep negatives in retail, wholesale and construction. Nonetheless, capacity utilisation remains above average and cost and price growth measures rose in the month – including retail price growth, which rebounded back up to 1.6% in quarterly terms.”

“This suggests that, while growth has slowed, the process of bringing supply and demand back into balance remains incomplete, reinforcing our expectation that inflation will continue to moderate only gradually from here.”

Midday market update

The ASX 200 has taken a tumble this morning, with the major benchmark down by -1.36% to 7,753.5 in trading so far today. Miners led the declines as investors awaited the US Federal Reserve’s policy meeting this week.

Gold miners, including West African Resources, Ramelius, St Barbara, and Bellevue Gold, saw significant losses after gold prices dipped below $2,300 an ounce on Friday.

Property developers Mirvac and Stockland also fell more than 2%, and the big four banks were weaker.

Investors are cautious ahead of key US consumer price data and the Fed rate decision later this week, where the central bank is expected to keep rates on hold but alter its projections to fewer rate cuts than previously forecast.

Traders have reduced expectations for US rate cuts following a strong US job report, with the market pricing in a 50% chance of a rate reduction in September, down from 70% before the data.

Australian bond yields jumped on the news, with three-year yields rising 9 basis points to 3.99% and the 10-year benchmark adding 10 basis points to 4.34%. Local traders imply a 30% chance of an RBA rate cut by Christmas and are fully priced for a move by July next year.

ANZ has pushed back the likely timing of the first rate cut to February 2025 from November this year and expects two more after that.

AGL Invests A$150 Million in Kaluza to Accelerate Electrification Efforts

Power company AGL Energy [ASX:AGL] is down by 2% so far today after announcing that it will acquire a 20% stake in Kaluza, a U.K.-based energy platform, for $150 million.

This investment is part of AGL’s plan to accelerate the electrification of its energy supply.

As part of the deal, AGL will migrate its 4 million electricity and gas customers onto the Kaluza platform. The company expects this move to result in annual pre-tax cash cost savings of A$70 million to A$90 million from fiscal year 2029 onwards.

AGL shares have only returned 4.37% in the past 12 months but more recently have upped their guidance and seen a civil case against them dropped.

ANZ Revises RBA Rate Cut Forecast

ANZ has revised its forecast for the first RBA interest rate cut, pushing it back from November 2024 to February 2025.

The bank says it anticipates two additional rate cuts following the initial easing.

Adam Boyton, head of Australian economics at ANZ, said today:

“We expect a follow-up easing shortly thereafter (most likely in April, although May is possible) and are retaining three cuts in our forecasts but see the final cut being delayed until the final quarter of 2025.”

This forecast joins others in suggesting that the RBA may maintain its current interest rate policy for a longer period than previously expected.

However, these bets have shifted wildly in recent months due to macro data, so we will see what happens next in our employment data.

In the US, we have a big macro week ahead, with inflation data out on Wednesday (AEST) and the upcoming Fed decision due Thursday evening (AEST).

Beach Energy Won’t Proceed with Project

Beach Energy [ASX: BPT] announced that it expects to recognise a non-cash impairment charge of approximately $365-400 million before tax in its FY24 full-year results. The impairment is related to issues in its Taranaki and Bass basins.

In the Taranaki Basin, the Kupe South 9 development well delivered low gas flow rates, leading to a reduction in expected recovery. This is expected to result in a non-cash impairment charge of approximately $115-125 million before tax.

In the Bass Basin, Beach has determined that development of there will not proceed as part of the upcoming Offshore Gas Victoria drilling program, saying ‘they do not meet minimum investment requirements’.

From this, Beach expects a non-cash impairment charge of approximately $250-275 million before tax for its Bass Basin assets.

For a full summary, Beach Energy’s FY24 full-year results will be released on 12 August 2024.

Beach’s shares fell on opening but have since recovered slightly and are up by +0.32% in early trading.

Morning market update

Good morning. Charlie here,

The ASX 200 opened down -0.87% to 7,791.4 this morning after catching up to a long weekend of market moves that has seen oil and bond yields climb while other commodities slid.

Hotter-than-expected US unemployment data pushed bond yields higher on Friday. US 2-year yields jumped 16bps to 4.89%.

Meanwhile, gold prices dropped over the weekend as China’s Central Bank released its latest report. They are recovering somewhat this morning but are still below their Friday close levels.

On Wall Street, markets closed slightly up on Friday, with the biggest news being Apple’s partnership with OpenAI to bring its AI onto its iPhones.

On the ASX, investors will be watching the bids fly as M&A begin to heat up as Bapcor confirms a $1.83 billion buyout offer from Bain Capital, while early speculation suggesting Strike Energy and Healius could also be attracting offers.

Wall Street: S&P 500 +0.26%, Dow +0.18%, Nasdaq +0.35%.

Overseas: FTSE -0.20%, STOXX -0.69%, Nikkei +0.92%, SSE flat.

The Aussie dollar +0.4% to US 66.10 cents.

US 10-year bond yields +3bps to 4.47%.

Australian 10-year bond +12bps to 4.34%.

Gold +0.5% to US$2,310.16, Silver +1.29% to US$29.71.

Bitcoin -0.17% to US$69,523, Ethereum -1.05% to US$3,665.

Oil Brent +2.84% to US$81.88, WTI Crude -0.44% to US$78.08.

Iron ore fell -3.1% to US$105.40 a tonne.

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988