ASX NEWS LIVE | ASX to Fall as Rate Cut Euphoria Fades; ACCC Sues Coles and Woolworths

Market close update

The Australian share market broke its seven-day win streak today, retreating from last week’s euphoric series of record highs as investors shifted their focus to tomorrow’s RBA meeting.

Growing concerns about a persistently tight job market and high inflation have raised fears that the start of the easing cycle could be delayed well into next year.

Analysts widely expect the central bank to maintain the cash rate at 4.35% for the seventh consecutive meeting and continue its firm stance on stubbornly high inflation.

The ASX 200 fell 0.69% to 8,152.9, moving away from Friday’s record close of 8,209.5.

8 out of 11 sectors finished in negative territory, with consumer-related stocks leading the downturn.

Supermarket giants Woolworths and Coles faced significant pressure after the competition regulator initiated legal action, alleging they had ‘significantly‘ violated the law by misleading consumers with discount claims on common products.

Coles shares dropped 3.6% to $18.59, matching its second-largest single-day decline this year, while Woolworths fell 3.3% to $33.79, marking its second-biggest daily drop in 2024.

Iron ore miners also experienced a gloomy session as prices of the steelmaking ingredient plummeted due to concerns about China’s economy. Index heavyweight BHP fell 1.3% to $39.81, and Rio Tinto lost 0.6% to $112.34.

In contrast, gold miners advanced as the precious metal’s price reached a new high of US$2,631.31/oz, driven by escalating tensions in the Middle East bolstering demand for safe-haven assets.

Ramelius shares rose 0.9% to $2.2, and West African Resources increased 1.5% to $1.72.

Uranium miners also had a strong showing, with Bannerman Energy up nearly 11% and Boss Energy climbing 8.2%.

This boost came on the heels of Microsoft’s mega-deal to revive a US nuclear plant, in which the tech giant committed to purchasing 100% of its power for 20 years.

China surprises with rate cut, signals further support coming

China’s central bank the PBoC has cut its short-term policy rate and announced a rare press conference, fueling expectations of increased economic stimulus.

The People’s Bank of China (PBOC) lowered its 14-day reverse repo rate, while also revealing plans for Governor Pan Gongsheng to address the media tomorrow.

These moves, coming shortly after the US Federal Reserve’s recent rate cut, suggest China may be preparing to boost efforts to revive growth.

The actions arrive amid concerns about meeting the country’s 5% annual growth target, especially following disappointing August economic data.

Market reaction has been swift, with bond yields falling as investors anticipate further monetary easing.

This combination of a rate cut and the scheduled high-level briefing indicates that Chinese officials are likely gearing up to implement more substantial measures to support the economy.

We’ll see what tomorrow brings but it could be worth watching major iron ore mining companies tomorrow.

RBA meeting concludes tomorrow, what to expect

The US Fed’s recent 50 basis point interest rate cut marks the beginning of a global monetary easing cycle that could see Australia left behind.

The Fed’s move signalled the end of pandemic-induced inflation and the hopes in many of a ‘soft landing’ scenario with modest growth and stable unemployment, allowing inflation to reach 2% by 2026.

In contrast, Australia is pursuing a divergent macroeconomic policy strategy. Many consider tomorrow’s interest rate decision to be almost certainly another ‘hold’ by the RBA.

Unlike most central banks, which prioritise inflation control through restrictive monetary policies, the RBA maintains a more neutral stance.

Meanwhile, rates have remained on hold since they were raised to 4.35% in November last year.

This approach aims to balance inflation risk with minimising negative impacts on employment. However its impact on households has been notable.

Recent employment data highlights the differences between the US and Australian economies. While the US labour market cools, Australia’s job market is booming, raising concerns about persistent inflation.

Total employment in Australia has grown significantly, with over 300,000 new jobs created this year.

Some view the RBA’s strategy as risky, worried that it may lead to more severe economic outcomes in the future.

However, the RBA remains committed to achieving price stability, albeit through a different approach than its global counterparts.

Tomorrow we will hear from the RBA board on its latest decision, as well as CPI data this week, which should give us insights into the country’s economic trajectory.

Uranium stocks lift on Microsoft plans

Uranium stocks on the ASX and Wall St are on the rise after Microsoft announced plans to revive the US-based Three Mile Island Nuclear plant.

Under the deal with Constellation Energy, Microsoft will buy 100% of its power for two decades to power its AI data centres.

Three Mile Island is well known for the 1979 incident, in which the facility faced a partial meltdown due to a mechanical failure in its liquid cooling system.

That was a separate reactor, and the remaining reactor remained in operation until 2019, when it was shut down for economic reasons.

When Three Mile Island was shuttered, it had a generating capacity of 837 megawatts, enough to power more than 800,000 homes.

Once brought back online, Constellation Energy said it expects to once again generate more than 800 megawatts of electricity for Microsoft.

This will be the first time a nuclear power plant has been reopened in the US after decommissioning.

On the ASX today we’ve seen strong gains from the major players, with:

Paladin Energy up by +6.50%

Deep Yellow up by +7.05%

Boss Energy up by +8.58%

Bannerman Energy +11.3%

Latest Fat Tail Daily Video

Here’s the latest from the new Fat Tail Daily video series.

Publisher James ‘Woody’ Woodburn is away, so this week, Fat Tail Daily editor Nick Hubble will join us to discuss the key trends and offer unique insights into market movements.

Today, Nick spoke with Crypto Capital and Alpha Tech Trader Editor Ryan Dinse.

Nick and Ryan discuss why Blackrock’s most recent report is urging investors to take action to protect their portfolios.

Is national debt something you should be concerned about? What do these record-high debt amounts mean for fiat currency?

Click below to watch the discussion.

Midday market update

The Australian stock market took a step back from its recent record high as investors grappled with the possibility that the RBA might delay its first interest rate cut until well into 2025.

Economists anticipate that the central bank will maintain its current cash rate of 4.35% at tomorrow’s meeting, marking the seventh consecutive hold, as it continues to focus on concerns about persistent inflation.

The ASX 200 dipped by 0.68% to 8,153.5 around midday. This decline follows Friday’s record-setting close of 8,209.5, which was fueled by the Fed’s surprisingly large 50bp rate reduction last week.

The market’s retreat was widespread today, with 8 of the 11 sectors posting losses.

Consumer-focused stocks, particularly the major supermarket chains, bore the brunt of the downturn.

Woolworths and Coles faced one of their most challenging trading sessions of the year after the competition watchdog initiated legal proceedings, accusing them of misleading shoppers with deceptive discount promotions on everyday items.

The selloff saw Coles shares tumble 3.6%, while Woolworths stock retreated 3.1%.

The mining sector also struggled as iron ore prices weakened. Industry heavyweight BHP saw its shares decline by 1.5%, and Rio Tinto stock slipped 0.6%.

However, South32 managed to buck the trend, gaining 0.5% following news that its Hermosa project in Arizona was in the running for $244 million in funding from the US Department of Energy.

In contrast, gold mining companies emerged as rare winners, buoyed by the precious metal’s price hovering near Friday’s historic peak. Ramelius shares climbed 2.1%, and Westgold rose 1.65%.

The banking sector was not immune to the downturn, with Commonwealth Bank shares dropping 1.3%.

The day’s most significant underperformer was Webjet, whose stock price plummeted by 12% thanks to a demerger of its successful B2C business, which has been renamed WEB Travel Group.

REA raises bid for UK’s Rightmove

Real estate listings giant REA Group [ASX:REA] has launched its third bid for UK rival Rightmove that values the British property listings company at £6.1bn ($11.9 billion AUD).

REA made the third bid overnight, lifting its offer to £7.70 a share, 9% higher than its initial approach.

Rightmove is a similar, huge property listing platform, and the combination of the two companies would make it a globally significant player in residential property listings.

Owen Wilson, chief executive of REA, expressed frustration that Rightmove’s board had not opened talks, saying:

‘We are genuinely disappointed at the lack of engagement by Rightmove’s Board and we strongly encourage the Rightmove Board to engage,’ he said in a statement.

REA shares are down by -0.65% in trading today at $197.70 per share.

Market bets on further jumbo cuts

While these probabilities are notoriously volatile, US traders are putting a 50% chance on another 50 basis points cut from the Federal Reserve at its next meeting.

A second ‘double cut’ was certainly not hinted at by the Fed itself, whose own dot-plot projections signalled a slower path down in the rate cut cycle.

Still, between now and the next FOMC meeting, we have two job reports and more economic data that could tip further into the weakness of the US economy.

The bulls and bears seem evenly balanced at the start of this week, with a sell-down on Friday and Today that could turn positive later this week.

For now, bearish news has found a bigger audience, with stories of further Chinese weakness as data on Friday showed local Chinese government bodies have cut spending while youth unemployment climbed to the highest levels this year.

Meanwhile, the People’s Bank of China (PBOC) has refrained from cutting lending rates, holding back the stimulus many in the market are hoping to see.

In the US, FedEX’s share price fell by 15% in Friday’s trading as the nation’s second-largest shipper disappointed investors with unexpected weakness.

US domestic shipping volumes fell by 3% as FedEx blamed weaker business-to-business demand.

The company then warned that business was expected to slow further by the end of the year. Some saw this as a troubling sign for the economy ahead.

Here’s an interesting chart tracking those cut expectations by Jim Bianco:

For the first time since the Fed cut last week, the market is pricing a better than 50% probability that they cut another 50 bps at the next FOMC meeting (Nov 7).

-151% = -100% fully prices a 25 bps cut, -51% for a 50 bps cut (negative = cut, positive = hike) pic.twitter.com/fBD5Rbnqm8

— Jim Bianco (@biancoresearch) September 23, 2024

Telix Pharmaceuticals acquires US-based RLS

Telix Pharmaceuticals [ASX:TLX] has acquired RLS, a US-based radiopharmacy network with 31 locations in America.

The deal was an upfront cash consideration of US$230 million plus an additional US$20 million based on certain milestones in the following four quarters.

The deal is expected to be cost-neutral for Telix from an operating cash flow perspective and will be funded through existing cash reserves.

RLS’s revenue for FY23 was US$158 million, and the company is already a distributor of Telix’s radio-diagnostic product, Illuccix.

The rationale behind the acquisition is the vertical expansion of Telix’s supply chain as it looks to expand its radiopharmaceutical products.

Dr Christian Behrenbruch, Telix Managing Director and CEO, said:

‘Our vision is to build a radiometal production and distribution network fit for the future. By combining the ARTMS platform and the RLS network, we can scale up the production of key isotopes and build a stable and consistent supply of PET and SPECT diagnostic tracers, along with therapeutic radiopharmaceuticals across the U.S. for the benefit of Telix, our partners and the patients we serve.’

Telix’s shares are down by -2.51%, trading at $19.80 per share today. In the past 12 months, the company has gained around 77%.

ACCC targets Coles and Woolworths over deceptive pricing

The Australian Competition & Consumer Commission (ACCC) has begun proceedings in the Federal Court against Woolworths and Coles supermarkets for allegedly breaching Australian Consumer Law by misleading consumers through discount pricing claims on hundreds of common supermarket products.

The ACCC allegations centre around selective price rises on products before brief periods of promotions, which would be lower than the price spikes, but higher than their regular pricing.

“We allege that each of Woolworths and Coles breached the Australian Consumer Law by making misleading claims about discounts, when the discounts were, in fact, illusory.”

“We also allege that in many cases both Woolworths and Coles had already planned to later place the products on a ‘Prices Dropped’ or ‘Down Down’ promotion before the price spike, and implemented the temporary price spike for the purpose of establishing a higher ‘was’ price,” Ms Cass-Gottlieb said.

The ACCC estimates that both supermarkets sold tens of millions of the affected products and ‘derived significant value’ from those sales.

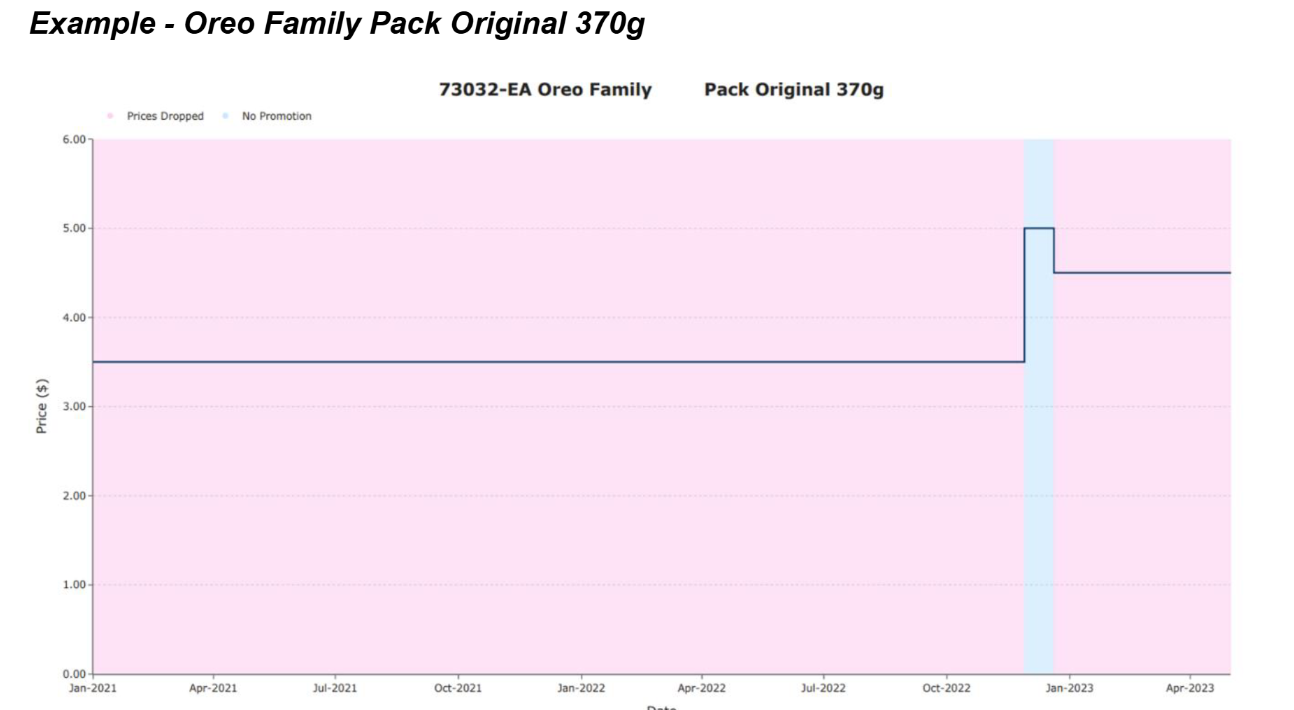

In its complaint today the ACCC gave examples like this to show how the deceptive pricing worked.

In the chart below, you can see the regular pricing of Oreos before a temporary price hike in December (in blue) before the product was advertised as ‘prices dropped’ but was, in fact, a higher price than the standard pricing.

Source: ACCC

In response to the allegations, Woolworths simply acknowledged the accusations and said it would ‘carefully review the allegations’.

Meanwhile, Coles attempted to blame the pricing changes on cost inflation, saying:

‘The allegations relate to a period of significant cost inflation when Coles was receiving a large number of cost price increases from our suppliers and, in addition, Coles’ own costs were rising, which led to an increase in the retail price of many products.’

‘Coles sought to strike an appropriate balance between managing the impact of cost price increases on retail prices and offering value to customers through the recommencement of promotional activity as soon as possible after the establishment of the new non-promotional price.’

Both Coles and Woolworth’s shares are down sharply in trading today, with Coles currently down by -3.66% and Woolworth’s down -4.3%.

Morning Market Update

Good morning. Charlie here,

The ASX 200 opened down -0.62% to 8,158.9 today, following Wall St and other major markets lower as the euphoria from the Fed’s rate cut last week fades.

In the US, markets still closed near best levels after a lower volume and choppy session on Friday.

A story hitting the news over the weekend was FedEx reporting much weaker earnings than the market was expecting.

Shipping companies are often considered ‘canaries in the coal mine’, so underperformance here was seen as a signal of trouble ahead for the economy.

Elsewhere, gold continues to climb higher, reaching a record high of over US$2,600 per ounce.

Uranium stocks also saw a strong lift on Friday on Wall Street as Microsoft announced plans to restart a nuclear facility.

On the ASX, the big news today will be that the competition regulator (ACCC) is suing Coles and Woolworths, alleging the two supermarkets have misled customers about discounts and products.

ACCC chairwoman, Gina Cass-Gottlieb explained the suit, saying:

‘Following many years of marketing campaigns by Woolworths and Coles, Australian consumers have come to understand that the ‘Prices Dropped’ and ‘Down Down’ promotions relate to a sustained reduction in the regular prices of supermarket products.’

‘However, in the case of these products, we allege the new ‘Prices Dropped’ and ‘Down Down’ promotional prices were actually higher than, or the same as, the previous regular price.‘

Also worth watching today, Fletcher Building is raising NZ$700 million in a fully underwritten NZ$282 million institutional placement.

| Name | Value | % Chg | |

|---|---|---|---|

| Major Indices | |||

| S&P 500 | 5,702 | -0.19% |

| Dow Jones | 42,063 | +0.09% |

| NASDAQ Comp | 17,948 | -0.36% |

| Russell 2000 | 2,227 | -1.10% |

| Country Indices | |||

| UK | 8,299 | -1.19% |

| Germany | 18,720 | -1.49% |

| Euro | 4,871 | -1.45% |

| Japan | 37,723 | +1.53% |

| Hong Kong | 18,258 | +1.36% |

| Name | Value | % Chg | |

|---|---|---|---|

| Commodities (USD) | |||

| Gold | 2,622 | +1.21% | |

| Silver | 31.17 | +1.33% | |

| Iron Ore | 90.60 | -1.17% | |

| Copper | 4.2672 | -0.44% | |

| WTI Oil | 71.03 | +0.05% | |

| Currency | |||

| AUD/USD | 68.06¢ | +0.02% | |

| Cryptocurrency | |||

| Bitcoin (USD) | 63,578 | +0.14% | |

| Ethereum (USD) | 2,581 | -1.42% | |

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988