ASX News Live | ASX Falls 0.5% As Markets Mull Over Rate Rises, Alphabet and Affirm Sink

US buy now, pay later Affirm cuts 19% of workforce, tanks in after hours trade

Large US buy now, pay later firm Affirm (NASDAQ:AFRM) will cut 19% of its workforce to cut costs as 2Q23 losses outpaced revenue.

It seems Affirm can’t escape the pressures the whole BNPL sector is under. Even PayPal (NASDAQ:PYPL) — who made a successful foray into instalment payments — announced job cuts last week.

Affirm’s workforce reduction comes after another quarter of net losses.

In the three months ending December 2022, Affirm’s revenue grew ~11% to US$400 million while operating expenses grew ~35% to US$759 million.

On an incremental basis, Affirm added about US$200 million in operating expenses to generate an extra US$39 million in revenue.

You’ve got to spend money to make money. But not like this. Selling a dollar for 20 cents isn’t sustainable.

In the 3 months ending December 2022, #BNPL fintech $AFRM's revenue grew ~11% to US$400m while operating expenses grew ~35% to US$759m.

On an incremental basis, Affirm spent an extra US$200m in operating expenses to generate an extra US$39m in revenue. pic.twitter.com/mVtTUEoHhp

— Fat Tail Daily (@FatTailDaily) February 9, 2023

Aussie BNPL stocks ended lower on Thursday, likely a despondent reaction to Affirm’s cash incineration and stock plunge.

- Zip (ASX:ZIP) finished 3.15% lower

- Sezzle (ASX:SZL) finished 8.5% lower

- Splitit (ASX:SPT) finished 2.6% lower

- Soon to be delisted Laybuy (ASX:LBY) finished 10% lower

P.S. From earlier this week:

https://www.moneymorning.com.au/20230207/is-this-the-end-for-asx-bnpl-stocks.html

Is there a pivot to real assets underway?

Our commodities expert James Cooper thinks mid-2022 marked a pivot in investor sentiment. A pivot from tech to real assets.

***

“Mid-2022 is a period that every investor and trader should take note of…while stock markets were panicking over US interest rate rises and spiralling inflation, strength was quietly building in key parts of the economy.

“I’ve pulled up two indices, one demonstrating strength, the other weakness at this all-important ‘pivot point’ in mid-2022:

Source: ProRealTime

“Following a major low in late June 2022, the Nasdaq 100 tech sector continued to post further lows in the second part of the year.

“This was the catalyst for strong bearish sentiment in equities across the globe.

“But not all stocks were performing poorly.

“Strength was emerging in what I believe will be the key areas of investment for the future.

“In stark contrast to the tech sector, the S&P ASX 300 Metals and Mining Index began to trend upward, despite the upheaval in markets throughout 2022.

“In my mind, the mid-point of last year signalled the beginning of a long journey toward a secular shift into real asset investments.

“As investors sold-off US-based growth equities, ‘higher lows’ began to form throughout the mining, energy, utility, and farming-related sectors.

“Importantly, the charts were signalling an emerging trend…something we would have missed had we relied on fundamental analysis alone.”

James Cooper | China is a far more important story than any recession

According to Business Insider, around half of China’s population now falls into the middle-class category.

Having sat in hiatus, it means a staggering 700 million Chinese now have the capacity to spend more…be it travel, housing, business growth, or investing.

For context, the US middle class also makes up around 50% of the population, or around 165 million people.

China now has the greatest share of middle-class earners on the planet, which arguably makes it the most underrated, yet important, economy for global growth.

Again, I don’t believe January’s rally has priced in the potential here.

Yes, we have US recession fears looming, but the China story is far more important, particularly from an Australian investor perspective.

It means a total shift in investor mindset is needed as China reignites its economic engines…and it’s the emerging economies that may be the unlikely winners this year. Let me explain…

With 700 million middle-class citizens now free to spend and travel, it means smaller Asian countries may soon host millions of additional Chinese travellers.

Enormous demand for flights and accommodation looks likely.

It could prove to be a boon for Australia’s travel industry too.

But that’s just part of the story when it comes to China’s economic ‘reawakening’…

https://www.dailyreckoning.com.au/prepare-for-the-great-reawakeningemerging-economies-set-to-rise/2023/02/09/

The newish tech frontier | Ryan Clarkson-Ledward

Excerpt from our editor Ryan Clarkson-Ledward’s latest piece for Money Morning

AI or artificial intelligence isn’t exactly a new phenomenon.

You’ve probably seen or heard about it for years at this point. Every other new fancy tech breakthrough is usually attributed to AI.

More often than not, this is just marketing hyperbole. Using simple algorithms or computer scripts isn’t what AI’s about, but it is easy to sell it as such.

Take ChatGPT, for example. You may have heard about this chatbot recently as it’s made numerous headlines of its own.

Apparently, it has become a popular tool among students to use the software to write essays. It has even been reported to have passed law and business school exams, as well as Google’s own coding interview.

In other words, it’s a highly sophisticated chatbot.

Is it the kind of society-breaking AI that you always hear about though?

No.

Not yet, anyway.

ChatGPT is still, for the most part, just a simple tool for written responses.

The easiest way to think about it is as if it’s a calculator for words instead of numbers. You provide it with a problem, and it will provide a solution.

The key difference, of course, is that words have far more nuance than numbers. Which is why ChatGPT is still an imperfect tool at the moment.

Just like Google’s ‘AI’, it can offer up factually wrong information. That’s what makes Google’s US$100 billion mistake so ironic. Because the main reason it was punished so heavily is because investors are worried that their main competitor, Microsoft, is pulling ahead in this AI race.

For all I know, they might be, but considering that Microsoft has invested heavily in the company behind ChatGPT, I don’t think Google is out of this race just yet…

https://www.moneymorning.com.au/20230209/bad-ai-just-cost-google-investors-us100-billion.html

In the long run, everything is a toaster

Business professor Bruce Greenwald — whose value investing course at Columbia got Warren Buffett’s seal of approval — once quipped that in the long run, everything is a toaster.

That is, in the long run, any competitive edge or innovation gets copied and competed away until prices plummet and it becomes a commodity as mundane as a toaster.

It’s weird to say already, but the speed with which competitors are rolling out their own ChatGPT tech suggests even something as high-tech as generative AI is slated to for the toaster treatment.

"In the long run, everything is a toaster."#ChatGPT #BardAI $BIDU $GOOGL $MSFT pic.twitter.com/vc69l1r40Y

— Fat Tail Daily (@FatTailDaily) February 9, 2023

Here’s a quick list of who is already offering (or is about to) generative AI products:

- OpenAI/Microsoft

- Alphabet

- You.com

- Perplexity

- Baidu

- Meta

- Apple (don’t forget the dominance of the Safari browser on iPhones)

This technology is set to lower margins for Internet search, especially. That’s not me guessing, that’s Microsoft boss Satya Nadella stating. Nadella said in an interview with the Financial Times that Microsoft is coming for Google’s margins — and it’ll happily shrink them to cripple a rival:

“From now on, the [gross margin] of search is going to drop forever. There is such margin in search, which for us is incremental. For Google it’s not, they have to defend it all.”

Commonwealth Bank raises savings … and variable interest rates

That didn’t take long.

The Commonwealth Bank has responded to the Reserve Bank of Australia’s 25 basis point cash rate hike.

Commbank’s home loan variable rates will rise by 25 basis points per year.

To lessen the blow, Commbank is also raising its GoalSaver savings rate by 75 basis points to 4%.

Changes to the variable rates will take effect on 17th of February.

Following the RBA’s decision to raise the official cash rate by 0.25% p.a., we will be making a variety of interest rate changes. 🧵

— CommBank (@CommBank) February 8, 2023

Megaport rises sharply than falls just as fast on half-year results

Telco stock Megaport (ASX:MP1) — the ‘most exciting tech adventure of this decade‘ — is currently down over 5% after jumping as much as 7% at the open on Thursday.

This intraday volatility is certainly an adventure of sorts, as investors digested Megaport’s half-year results.

The stock is down 55% over the past 12 months and fell sharply last week on the release of its 2Q23 update.

Today, Megaport’s released half-yearly showed revenue rose 27% to $47.4 million while net loss after tax shrank 37% to $9.2 million. Megaport also stemmed its free cash flow losses. Negative free cash flow improved from $28.8 million to $13.7 million YoY.

Megaport saw its cash and cash equivalents fall to $39.2 million at the end of the period.

On a key metrics basis, the half-year performance is solid YoY. But the performance from half to half highlights a slowdown in enabled data centres, cloud onramps, customers, and ports.

Source: Megaport

#MP1 is down 5% on its 1H23 results.

While #Megaport stemmed losses, it continued to burn cash.

Cash & cash equivalents at the end of 1H23 shrank to $39.2m from $76.0m YoY. #ASX #ausbiz pic.twitter.com/9RXvthSjP8

— Fat Tail Daily (@FatTailDaily) February 9, 2023

US stocks still look historically pricey

Robert Shiller is a Nobel-winning economist who popularised what’s now called the Shiller Cyclically Adjusted Price Earnings (CAPE) ratio.

The CAPE ratio divides the US benchmark S&P 500 index’s current price by the 10-year moving average of inflation-adjusted earnings.

Using the CAPE ratio and a trust in mean reversion, investors can see the likely direction of the market.

A higher CAPE ratio could reflect lower returns over the next decade and a lower CAPE ratio could reflect higher returns over the next decade as the ratio regresses to the mean.

The current CAPE ratio is an elevated 29x. Well down on a year ago, but still historically high. The median CAPE ratio is about 16.

Source: Multpl.com

Just a reality check on buying the S&P at these levels for anything more a 'trade'. Shiller Cyclically Adjusted Price Earnings (CAPE) valuations are still at 29x… If you are 'buying the dip' or buying 'Stocks for the Long Run' then time is not on your side at these valuations pic.twitter.com/dY76uo6X03

— Ian Harnett (@IanRHarnett) February 2, 2023

Uber rises after revenue growth but continues to burn cash

Uber was the poster child for the aggressive growth company who relegated profitability to the back burner.

Market share and mindshare — that’s all that mattered.

Until things like free cash flow became cool again.

In May 2022, Uber CEO Dara Khosrowshahi messaged staff saying the market is shifting and ‘we need to show [investors] the money:’

We have made a ton of progress in terms of profitability, setting a target for $5 billion in Adjusted EBITDA in 2024, but the goalposts have changed. Now it’s about free cash flow. We can (and should) get there fast.

Their questions run the gamut from, “Has anyone other than you made money in on-demand transport?” to “Ridesharing has been around for awhile, why isn’t anyone else profitable?” They see how big the TAM is, they just don’t understand how that translates into significant profits and free cash flow. We have to show them.

Is Uber finally starting to show investors it can translate its massive TAM into profits?

Uber’s 4Q22 revenue grew 49% YoY to US$8.6 billion leading to net income of US$595 million. The ride-hailing and delivery business grew its incremental margin to 10%.

Khosrowshahi told shareholders:

“We ended 2022 with our strongest quarter ever, with robust demand and record margins. Our global scale and unique platform advantages position us well to accelerate this momentum into 2023.”

But not all were taking the bait.

FT’s Lex column noted after the results release:

“Investors in Uber want to know whether the core business of rides and food delivery can be profitable on a sustainable basis. Uber says non-GAAP metrics allow for more transparency. But the huge variation between adjusted ebitda and net income creates confusion. There is no standard definition of adjusted ebitda either, making it hard to compare one company with another.”

4Q22 free cash flow (as defined by Uber) was a negative US$303 million, up from a negative US$187 million the previous year. That said, free cash flow (as defined by Uber) was positive over the 12 months to December 2022, coming in at US$390 million. A huge improvement on negative free cash flow of US$743 million in the twelve months to December 2021.

Yet the actual, unadjusted free cash flow tells a different story.

If we look at Uber’s actual statement of cash flows, we see that free cash flow for the 12 months to December 2022 was negative US$995 million. Cash and cash equivalents fell by US$1.1 billion in the year.

12 months to December 2022 net decrease in cash & cash equivalents — US$1.1 billion. pic.twitter.com/gncqhCJP7Y

— Fat Tail Daily (@FatTailDaily) February 8, 2023

Alphabet’s BardAI $100 billion dollar hiccup

Alphabet — parent of Google (is this elaboration as tedious to read as it is to type out?) — fell 8% overnight. Its ChatGPT rival, BardAI, inputted a factual error … on debut.

If your AI product is spotted to have errors during a promotional unveiling video, you’ve at least got some PR problems. Especially when your rival’s AI product is signing up users at a historic pace.

A video demo of BardAI’s capabilities showed Bard (I like Bart or Burt better) answering a question about new discoveries assisted by the James Webb Space Telescope.

Bard said the telescope ‘took the very first pictures of a planet outside of our own solar system’.

Wow, I didn’t know that. That’s pretty cool, thanks, Burt.

Except Bard was wrong, and astronomers were incensed.

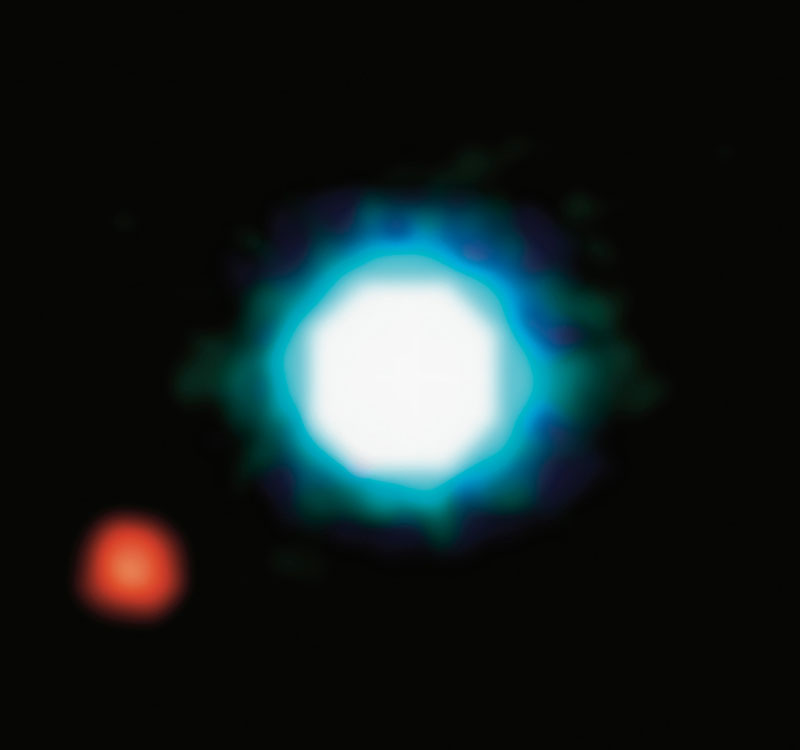

On its website, NASA says the first image of an exoplanet was taken in 2004 by a different telescope.

That’s the exoplanet below.

Source: NASA

Here’s how NASA described it:

“This composite image shows an exoplanet (the red spot on the lower left), orbiting the brown dwarf 2M1207 (centre). 2M1207b is the first exoplanet directly imaged and the first discovered orbiting a brown dwarf. It was imaged the first time by the VLT in 2004. Its planetary identity and characteristics were confirmed after one year of observations in 2005. 2M1207b is a Jupiter-like planet, 5 times more massive than Jupiter. It orbits the brown dwarf at a distance 55 times larger than the Earth to the Sun, nearly twice as far as Neptune is from the Sun. The system 2M1207 lies at a distance of 230 light-years, in the constellation of Hydra. The photo is based on three near-infrared exposures (in the H, K and L wavebands) with the NACO adaptive-optics facility at the 8.2-m VLT Yepun telescope at the ESO Paranal Observatory.”

Alphabet fell by the most in more than three months after a demonstration of its new AI chatbot, Bard, sparked some concerns.

Bloomberg's @EdLudlow reports with more details https://t.co/WhcD3cA5AN pic.twitter.com/EBPjO5GEaG

— Bloomberg Technology (@technology) February 8, 2023

Good morning, investors

Good morning.

Will today be another eventful day in the markets? Let’s find out.

As always, some stocks are set to rise, some set to fall. But all the while, we hope to glean some insights along the way.

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988