ASX News LIVE | ASX to Fall Ahead of Aus Inflation Data; Nvidia Rebounds

Market close update

The ASX 200 closed down -0.71% to 7,783.0 in a volatile session that saw a broad selloff after the latest monthly inflation numbers spiked.

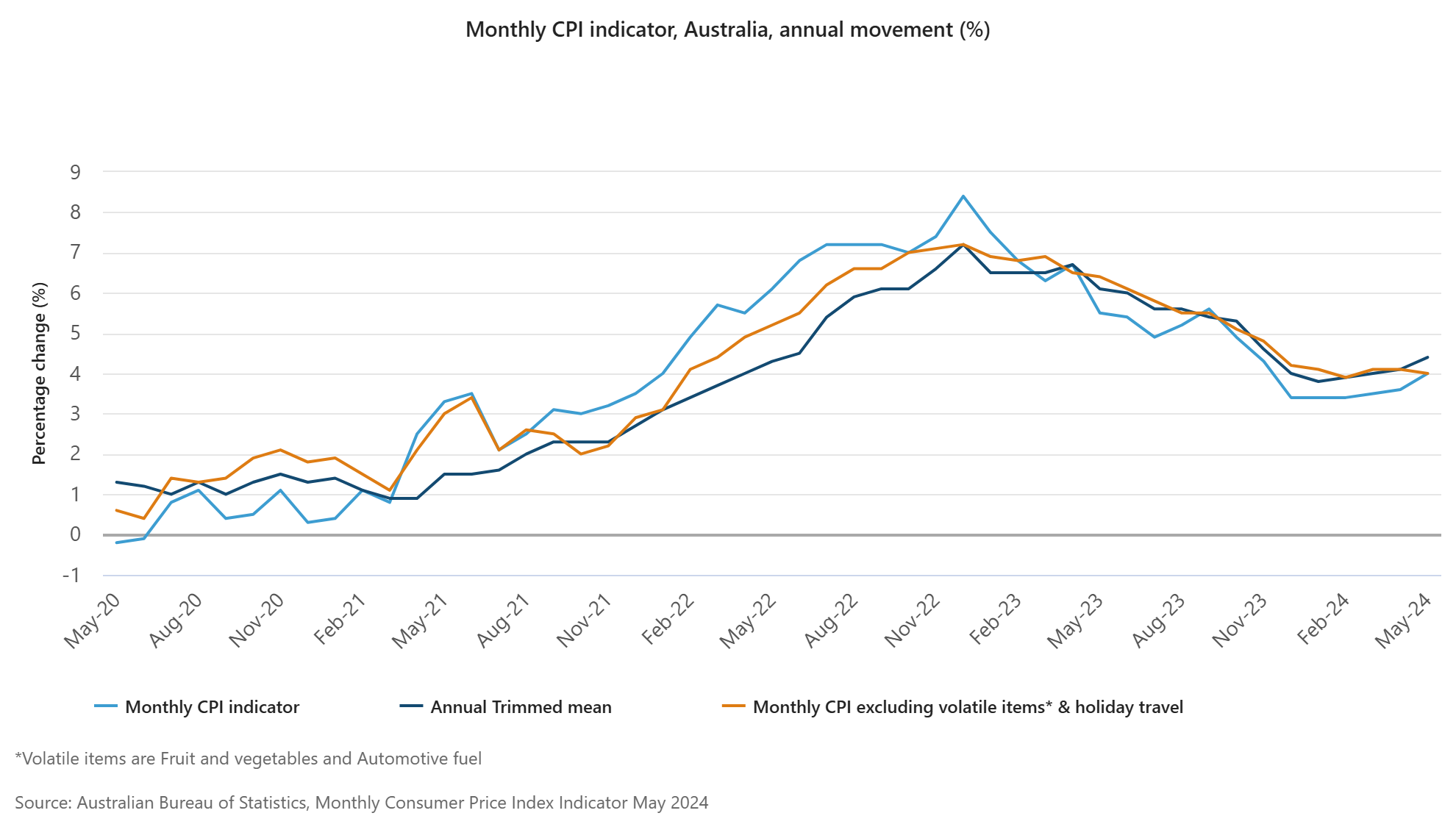

May CPI figures showed inflation hitting 4%, that was up from April’s 3.6% and well above the expectations of 3.8%.

Interest rate sensitive sectors like real estate (-2.04%), banking (-0.94%), and consumer discretionary (-1.46%) all dipped after the CPI numbers.

Only tech (+0.77%), energy (+0.53%), and utilities (+0.25%) were spared from the worst of the brunt today, following similar gains seen on Wall Street overnight.

After the figures, many economists (see comments in the previous post) are now predicting that the RBA’s August meeting is now ‘Live’ and could potentially be a rate rise.

That puts us as an outlier amongst the G10 countries as the only country where underlying inflation has risen since December and puts us at the back of the queue for rate cuts, whenever they eventually come.

We’ll see how the markets react to the RBA’s stance when we hear from Deputy RBA Governor Andrew Hauser tomorrow at the Australian Economic Forum.

Until then, have a great evening.

August RBA meeting now ‘Live’

Many economists and traders have weighed in on today’s hotter-than-expected CPI data, which came in at 4.0%, above the 3.6% last month and above the estimates of 3.8%.

The August meeting is now well and truly ‘Live’ in the eyes of many economists, that is, the chance of a rate hike is now well in play.

Let’s go through some of the comments we’ve seen so far today:

Deutsche Bank is now predicting a hike in the August meeting, with its chief economist Phil O’Donoghue saying:

“Underlying inflation is intolerably high in Australia. In fact, Australia is the only G10 country where underlying inflation has increased since December,”

“If the complete suite of price updates for Q2 looks a little more benign than the monthly indicator suggests, then there is still a chance that the RBA will hold fire.”

“With GDP growth in fact falling short of the bank’s forecasts, we think the bank will take the upside surprise in its stride, though we still think it will cut interest rates only in Q1 2025 rather than in Q4 this year as most anticipate.”

“The upshot of today’s result is that it places enormous pressure on the Reserve Bank to not only not cut interest rates anytime soon, but potentially lift them further.”

“We weren’t expecting the RBA to cut rates until the second half of 2025, but the hotter-than-expected CPI print today indicates this could be even further away,”

“Forget ‘higher for longer’ – we may end up being the ‘highest for the longest.”

Fall in lithium price hits ASX hopefuls

Lithium stocks are among the bottom performers on the ASX today as Chinese lithium prices continue to fall.

Lithium carbonate futures are down 5% to US$12,000 a tonne today, that’s now down slightly under 15% in the past month alone.

This has been a very red day for micro and small-cap lithium explorers on the ASX, while some of the mid-caps have recovered from their morning losses.

Pilbara Minerals remains the ASX’s most shorted stock, with 20.6% of its stock shorted, well above the runner up Idp Education at 13.5%.

Citibank blamed the lithium price fall on rising inventories, with estimates of an increase of ~70,000 tonnes in the year to date.

Citi analyst Shreyas Madabushi commented, saying:

“This high and rising low-shelf-life chemical inventories should see lithium prices fall another 15 to 20 per cent to $US10,000 a tonne on GFEX, and CME hydroxide prices drop to $US10,000 a tonne over the coming months.”

“Prices around these levels are expected to eventually lead to mine/converter closures and industry rationalisation.”

Bannerman Energy Goes Into Halt Before Raise

Uranium developer Bannerman Energy [ASX:BMN] is in a trading halt today pending a capital raise.

The company is known for its Flagship Nambian Etango Project, which is slated to begin full production near the end of 2026.

The full details of the latest investor presentation can be found here for those interested.

Before the halt, shares were trading at $3.58 per share and have gained 137.8% in the past 12 months.

Midday market update

The ASX 200 is down by -1% trading at 7,759.0 after a hotter than expected CPI data (see last post for more details) derailed the markets.

Just look at that market reaction at 11:30 am.

Source: TradingView

After the report, which you can read in full here, only Information Tech (+0.28%) sector remains in the green.

This is helped by the recovery of Nvidia and the Nasdaq overnight as well as strong performances by Megaport (+1.37%), Novonix (+4%), and Brainchip (+6.25%).

Meanwhile, this morning’s laggard was yesterday’s darling, KFC operator Collins Foods, which is down by -7%, reversing all gains seen yesterday as the share price spiked after a strong FY24 report.

Latest inflation data comes in hot, ASX drops

The ASX has plummeted after the latest monthly CPI data from the Australian Bureau of Statistics.

The monthly inflation indicator rose 4.0% in annual terms, that’s up from 3.6% last month and above market expectations of 3.8%.

The most significant price increases were seen in Housing (5.2%), Food and beverages (+3.3%), Transport (+4.9%), and Alchohol and Tobacco (+6.7%).

Source: ABS

While some items like meat and seafood (-0.6%) and Gas (-3.9%) saw deflation, the overall picture was one of rising costs.

This is precisely what the RBA did not want to see this month and could mean rate rises come back into the picture of possibilities (around a 1 in 5 chance of a raise)

So its hold or hike now for the RBA, with interest rate cuts well out of the picture.

With tensions on the Israeli and Lebanon border increasing (threatening higher oil prices) and shipping costs continuing to surge, we could see further inflation down the track.

Brainchip tops the ASX this morning

Brainchip Holdings [ASX:BRN] ‘s share price jumped +6.25% this morning after a Pitt Street investor report outlining the company came out yesterday.

You can read the full report here, but it is worth noting that Pitt works on a commission basis so it was paid by Brainchip to produce the report.

While I have only skimmed the report in truth, I remain a tad sceptical of the lofty $1.59 per share valuation. Brainchip is currently at around 21 cents per share and has seen its trading volumes and share price slide since a spike in February.

Pitt says they arrived at their valuation based on a parallel M&A example of a buyout deal by Intel for an Israeli startup called Habana in 2021.

As always, I encourage you to do your own research before any investment; I just felt that context is important for the ASX leader so far today.

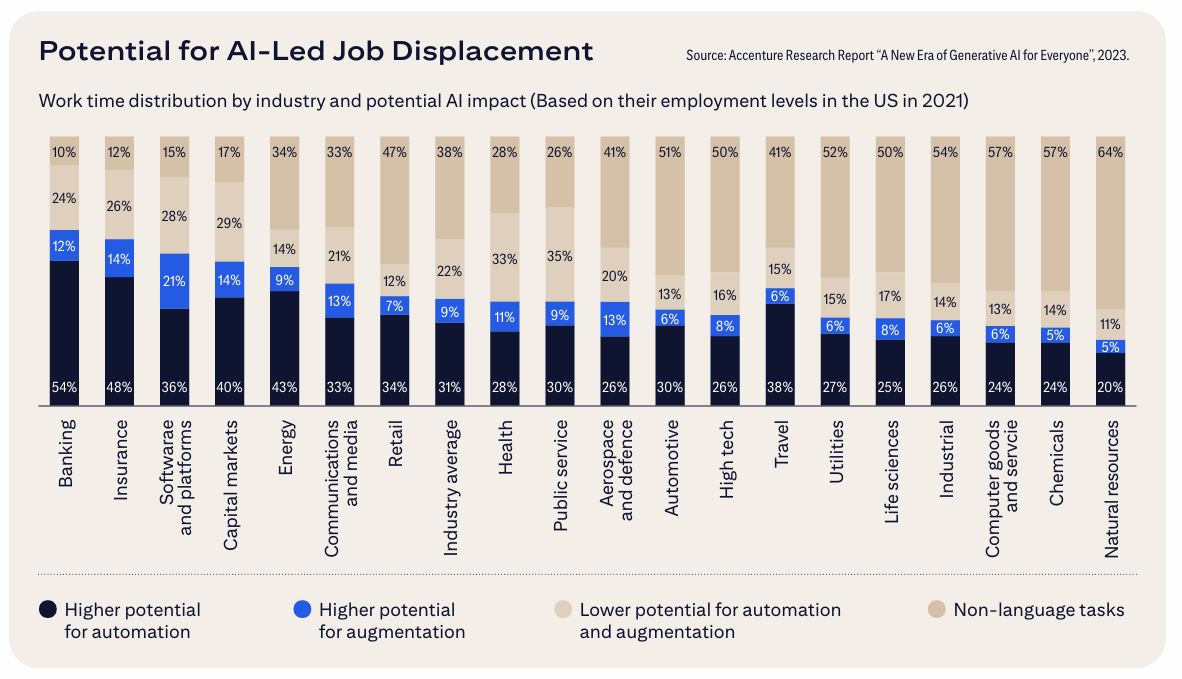

Is AI coming for your job?

In the latest deep report from Citigroup, which you can read in full here, the investment bank outlines its future projections for AI in finance.

The key takeaway: AI is coming for finance jobs.

The company listed Banking, Insurance, and software developers as the top segments likely to see job losses in the near term.

For now, that will likely centre around things like sales, fraud detection, document processing, credit decisions, pricing for bankers and insurers.

Here is the key chart showing which sectors have the potential for the most ‘displacement’ in the shorter term.

Source: Citigroup- Accenture Research

Morning market update

Good morning. Charlie here,

The ASX 200 opened down by -0.63% to 7,789.4 this morning as traders remain cautious before the monthly inflation data due at 11:30 am AEST.

On Wall Street, the S&P 500 and Nasdaq recovered from their three-day drop following Nvidia as it bounced +6.7%.

Many of the Fed president’s speeches this week have centred around concerns about unemployment levels, with some warnings of a spike around the corner, while some say it could be needed to squash inflation.

Meanwhile, in Canada, inflation surprised upward this month for the first time in five months, putting many markets on watch.

In Japan, the expected Yen intervention never materialised overnight, but traders are still expecting a move here.

On the ASX, we await the CPI data at 11:30 am AEST, so stay tuned for that and market reactions here.

Wall Street: S&P 500 +0.39%, Dow -0.76%, Nasdaq +1.26%.

Overseas: FTSE -0.41%, STOXX -0.30%, Nikkei +0.95%, SSE -0.44%.

The Aussie dollar -0.11% to US 66.45 cents.

US 10-year bond yields +1bps to 4.24%.

Australian 10-year bond -2bps to 4.19%.

Gold -0.5% to US$2,319.5, Silver -2.27% to US$28.85.

Bitcoin +2.41% to US$61,733, Ethereum +1.12% to US$3,390.

Oil Brent -1.24% to US$84.94, WTI Crude -0.11% to US$80.74.

Iron ore +0.5% to US$103.05 a tonne.

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988