ASX News Live | ASX Falls After US Stocks Record Worst Day In Weeks

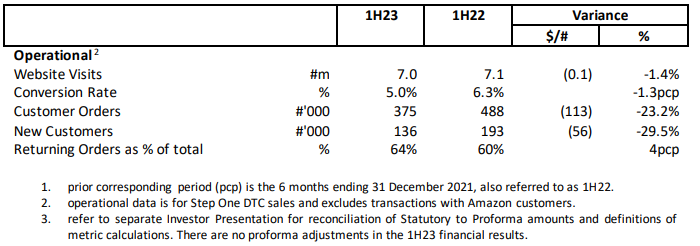

Step One rises 17% on 1H23 results

Step One Clothing (ASX:STP) — the direct-to-consumer underwear merchant down over 80% since listing in November 2021 — closed up big today on the release of its 1H23 results, bucking the wider market.

While revenue dipped 6% to $36 million, half-year profit rose nearly 240% to $5 million largely due to reduced marketing spend and 1H22 impacted by $4 million worth of listing and cap raise fees and $6.5 million worth of share-based payment expenses.

Step One said the revenue decline was deliberate as it ‘focused on business profitability in preference to revenue growth in this reporting period’.

While net profit jumped, gross profit as a percentage of revenue fell to 80.7%, down from 1H22’s 83.1%.

Total customers rose by 136,000 to 1,237,000, a 12% increase on the prior relevant half. The customer growth has slowed, however, as 1H22 saw 193,000 customers added.

Step One said it attracted over 7 million website visits in the half with an average conversion rate of 5%. This was down on 1H22’s website visits of 7.1 million and average conversion rate of 6.3%.

In all, its operating business metrics weren’t stellar and may reflect the 20% cut in marketing spend.

Undies merchant $SPT closed 17.7% higher on Wednesday on 1H23 results.

While revenue and gross profit margin fell, Step One swung back to a net profit, largely thanks to reduced marketing spend and 1H22 containing $4 million worth of listing and cap raise fees. #ASX #ausbiz pic.twitter.com/dBUdSAjm7t

— Fat Tail Daily (@FatTailDaily) February 22, 2023

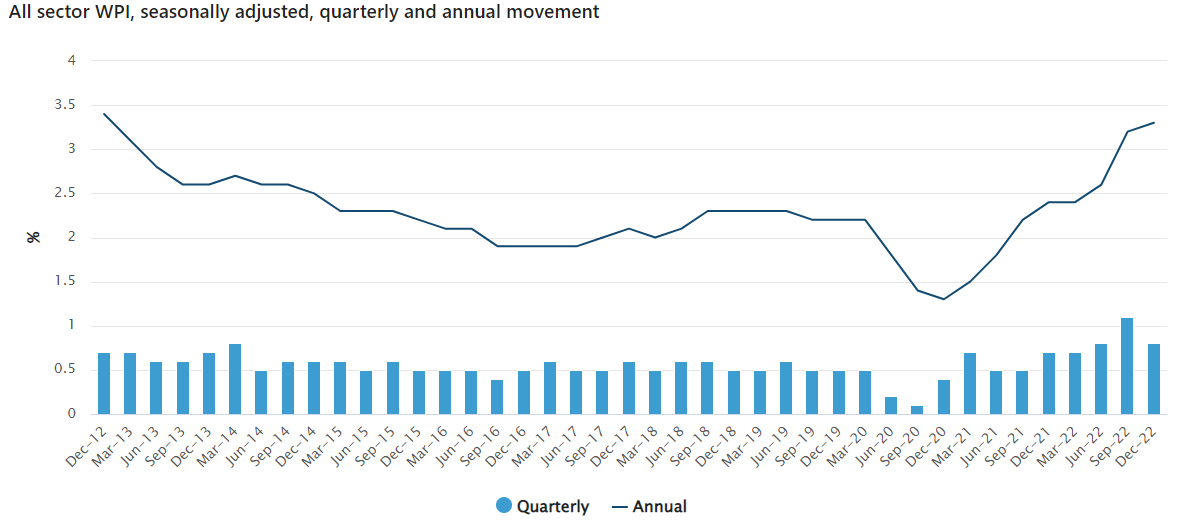

Australia’s wage price index rises to decade-high but wages growth still negative in real terms

Australia’s wage price index rose 0.8% in the December quarter and 3.3% over the year, a decade high.

Wages growth was softer than markets expected, though, and traders are already making bets the Reserve Bank will lower its peak cash rate to 4.2%.

Wages growth even undershot the RBA’s own 3.5% forecast.

Despite rising to a decade high, wages growth is still negative in real terms, with the December quarter headline inflation rising 7.8% YoY.

Source: ABS

Australian Bureau of Statistics’ Michelle Marquardt commented on the latest data:

“The increase in hourly wage rates for the December 2022 quarter was lower than the increase for the September quarter (0.8 per cent compared to 1.1 per cent). It was, however, higher than any December quarter increase across the last decade. This follows on from the September and June 2022 quarters which were also higher than their comparable quarters back to 2012. In combination these quarterly increases have resulted in the highest annual growth in hourly wages since December quarter 2012.”

The latest wages data has quickly percolated through the market and participants are reassessing their bets on the terminal rate of interest rates.

Commonwealth Bank, however, is sticking to its base case, with CBA’s Gareth Aird saying:

“We retain our base case that the annual rate of wages growth will peak at 3.8 per cent in mid‑2023. We do not share the RBA’s central scenario that the annual rate of wages growth will lift to 4.2 per cent. As such, we expect inflation to subside more quickly than the RBA.

Today’s report should be interpreted as good news. On one hand, it may not seem as such given real wages are deeply negative. Workers in Australia have gone backwards. But the wages dynamics right now in Australia mean that the RBA can pursue their objective of keeping the economy on an ‘even keel’.

The RBA does not need to generate a meaningful lift in the unemployment rate to bring inflation down given wages growth is consistent with the inflation target. The lagged impact of the already delivered rate hikes will slow the economy in 2023 and inflation pressures will abate.

There is still a very large number of home borrowers that will roll off ultra‑low fixed rate home loans onto significantly higher mortgage rates in 2023. This means there is more tightening to come for the Australian household sector irrespective of how much higher the RBA takes the cash rate. There is a key risk now that the RBA is tightening policy into a labour market and economy that is already showing sufficient signs of softening.”

RBA’s cash rate lags peers

The Reserve Bank of New Zealand’s latest cash rate increase has highlighted just how behind our own central bank is compared to peers.

RBNZ’s cash rate now stands at 4.75%.

The US Fed’s rate stands at 4.50% to 4.75%.

The Bank of Canada’s policy rate stands at 4.50%.

The Bank of England’s current rate is 4%.

The Reserve Bank of Australia’s, on the other hand, is at 3.35%.

Is our economy really that special? Are we really insulated more than comparable economies from inflationary pressures?

The RBA board’s February meeting minutes released yesterday show the central bank is aware of the disparity and offered some explanations:

“Members also noted that the cash rate was lower than policy rates in many other comparable economies. While wages growth remained lower here than elsewhere, Australia’s positive exposure to higher commodity prices and the extra savings buffers accumulated by households were estimated to be larger than in other countries. There were also notable differences in fiscal policy and population growth around the globe. Members observed that the cash-flow channel of monetary policy was stronger in Australia than in other countries, given the high level of variable-rate debt. But members also observed that, after taking account of all the channels for monetary policy transmission, there was little evidence to suggest that the overall impact of monetary policy on activity and inflation in Australia was materially different than elsewhere.”

RBNZ considered 75bp rate hike

The Reserve Bank of New Zealand considered raising the official cash rate to an even 5% from 4.25% but decided on a 50 basis point increase instead.

The central bank contemplated the big hike because inflation risk still skews to the upside.

However, the RBNZ decided on a smaller hike because the extent of the inflation risk has ‘moderated somewhat’ since November.

While the #RBA contemplated a 50bp hike and settled on 25bp, #RBNZ contemplated a 75bp hike and settled on 50pb. https://t.co/IhJMRbPNuO pic.twitter.com/8QwvlpQgy5

— Fat Tail Daily (@FatTailDaily) February 22, 2023

We mentioned the neutral interest rate earlier today and the concept popped up again in RBNZ’s February policy statement.

The central bank noted short-term inflation expectations are stubbornly high. These expectations imply the nominal neutral interest rate is rising.

So for RBNZ’s policies to be sufficiently restrictive, ‘interest rates need to increase by more to exert the same influence on the economy’.

NZ Reserve Bank ups rate 50bp to 4.75%, contemplated 75bp hike

The Reserve Bank of New Zealand has just increased the official cash rate from 4.25% to 4.75%. The last time New Zealand’s cash rate was higher was December 2008.

While the RBNZ saw early signs of price pressure easing, it concluded core inflation is still too high and employment still ‘beyond its maximum sustainable level’.

RBNZ said higher interest rates ‘are still needed to meet our inflation and employment objectives’.

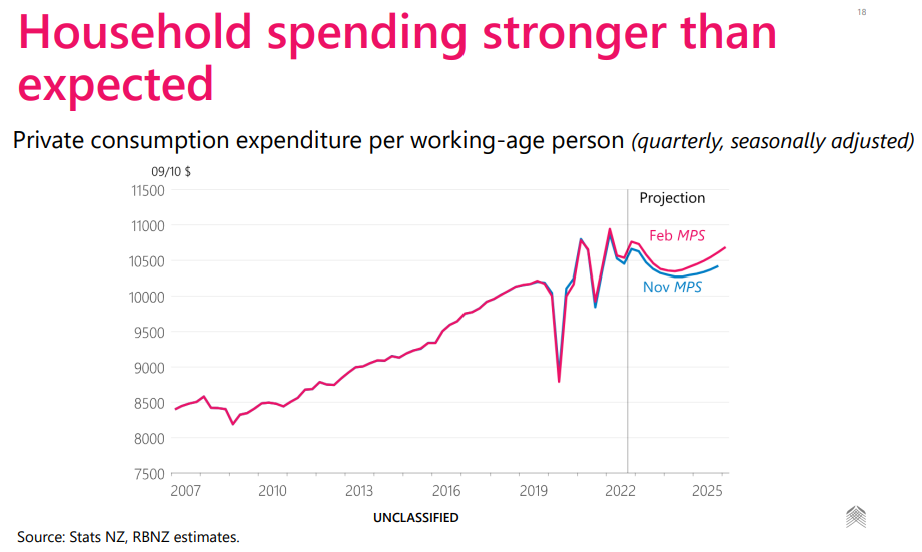

Household spending remains ‘stronger than expected’ with the central bank revising up its private consumption expenditure forecasts.

Source: RBNZ

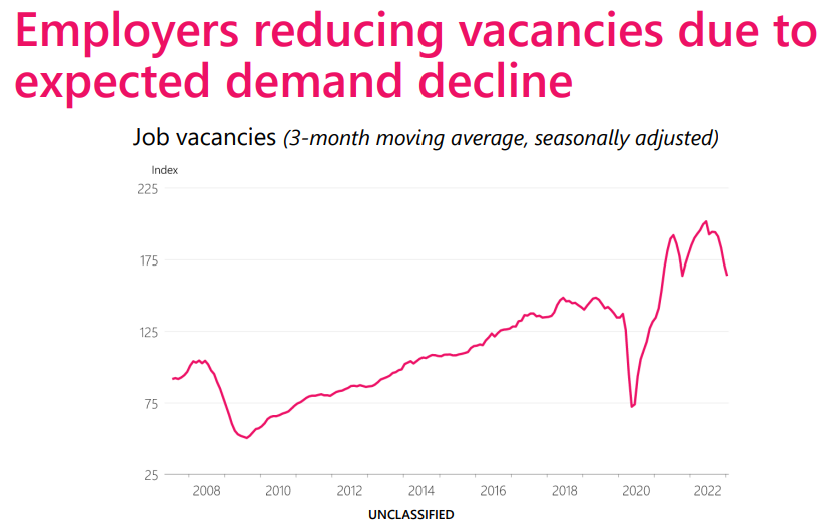

But the RBNZ is noticing signs of easing.

For one, employers are reducing vacancies in anticipation of falling demand.

Source: RBNZ

Why care about the natural interest rate?

‘The invention of debt and the emergence of interest to incentivise lending is the most significant of all innovations in the history of finance.’

Thus writes William Goetzmann in Money Changes Everything, his insightful tome on the history of finance.

Interest makes lending attractive. In turn, lending helps borrowers smooth their consumption and bring their future cash to bear on their present problems.

Well-greased, the economic machine starts turning.

An important upshot of interest, however, is its close relationship to the productivity of capital.

Imagine you’re a wealthy merchant in Mesopotamia called on by a farmer to lend him x amount of money to cultivate a farm.

You could lend him the money with interest, or you could buy the land yourself and cultivate it.

If the gain from cultivating the land far exceeds the gain from charging interest, you will not lend.

Therefore, the interest charged must have some relation to the productivity of the capital extracted with the help of the loan.

Nicholas Barbon summarised this idea in the 17th century by saying that ‘Interest is the rent of stock (i.e: capital), and is the same as the rent of land.’

This connection to the fruit debt bears is very important.

Modern finance can make interest seem like an abstruse concept abstracted away from anything tangible. But that is far from the case.

As economic historian Edward Chancellor wrote in The Price of Time:

‘Interest has always been with us because resources have always been scarce and must be rationed somehow, because wealth is unequally distributed between creditors and borrowers, and because, as Bohm-Bawerk says, “interest is the soul of credit.” Interest exists because loans are productive, and even when not productive still have value. It exists because those in possession of capital need to be induced to lend, and because lending is a risky business.’

The etymology of interest itself hints at the thrust of the argument so far.

Goetzmann notes in his book that the word for interest in ancient Greek, tokos, refers to the progeny of cattle. The Egyptian word for interest, ms, means ‘to give birth’.

As Goetzmann summarises (emphasis added):

‘All these terms point to the derivation of interest rates from the natural multiplication of livestock. If you lend someone a herd of thirty cattle for one year, you expect to be repaid with more than thirty cattle. The herd multiplies—the herder’s wealth has a natural rate of increase equal to the rate of reproduction of the livestock. If cattle were the standard currency, then loans in all comparable commodities would be expected to “give birth” as well. And that brings me to the neutral rate of interest.’

And that leads us to the natural rate of interest.

https://www.moneymorning.com.au/20230221/why-you-should-care-about-the-neutral-rate-of-interest.html

Canadian inflation fell more than expected

Canadian inflation fell by more than expected — a welcome reverse of recent inflation readings.

Canada’s CPI rose 5.9% year over year in January, down from a 6.3% increase in December. January prices rose 4.9% year on year excluding food and energy, also down on December.

Month on month, however, the CPI rose 0.5% in January following a 0.6% decline in December.

Statistics Canada said higher gasoline prices and rising mortgage interest costs contributed the most to the month on month increase.

Announcing the latest inflation data, Statistics Canada warned about base rate effects:

“In the first half of 2022, the global economy was significantly affected by the Russian invasion of Ukraine, and Canadian consumers experienced a significant increase in prices from January to June 2022. Headline consumer inflation increased from 5.1% in January to 8.1% in June 2022. The broad increase in prices in the early months of 2022, led by energy products, had a downward impact on the year-over-year rate of consumer inflation in January 2023, because higher prices from January 2022 were used as the basis for year-over-year comparison.

Price increases observed in the first half of 2022 will continue to fall out of the 12-month price movement. While inflation has slowed in recent months, prices remain elevated. Users should consider the impact of base-year effects when interpreting the 12-month price movement.”

Canadian inflation fell more than expected in January supporting the case for the BoC to pause rate hikes.

(EvercoreISI chart) pic.twitter.com/2qhcYXpGOc— Shane Oliver (@ShaneOliverAMP) February 21, 2023

’50 basis points’ the clue to recent gloom

Why are markets suddenly souring?

The Cboe Volatility Index (VIX) is up over 15% in the past five days alone! The higher the VIX, the higher the level of fear in the market.

So, why?

50 basis points.

While both the US Fed and our Reserve Bank raised interest rates by 25 basis points in their most recent meetings, both banks contemplated raising rates 50 basis points.

The contemplation of a 50 basis point hike implies central banks are nowhere close to pausing — let alone cutting — interest rates.

That means we’re likely stuck with high interests for longer.

Last week, Cleveland Fed president Loretta Mester gave a speech in Florida. Mester said that in the February FOMC meeting, she saw a ‘compelling economic case for a 50-basis point increase, which would have brought the top of the target range to 5%.’

And yesterday, the RBA released its February board meeting notes.

The RBA board said it considered two options — a 25 basis point increase and a 50 basis point increase. Explaining the argument for a 50 basis point hike, the RBA board said:

“The arguments for a 50 basis point increase stemmed from the concern that there had been a pattern of incoming prices and wages data exceeding expectations, and a risk that high inflation would be persistent. If it did persist, there would be significant costs, including higher interest rates and a larger increase in unemployment later on. Relatedly, members observed that the longer inflation stayed high, the greater the risk of price and wage expectations moving higher.”

$RBA board members considered raising the interest rate by 50 basis points in the February meeting. #auspol #ausbiz pic.twitter.com/aSltWihKV9

— Fat Tail Daily (@FatTailDaily) February 21, 2023

Morgan Stanley: recent S&P 500 rally ‘pure FOMO’, earnings forecasts too high

“This is pure FOMO at its best, in our view, and we find all the hoopla and excitement about the rally to be misplaced”.

So wrote Morgan Stanley’s Mike Wilson in a research note overnight.

Wilson continued:

“The reality is that the S&P 500 is flat over the past 11 weeks and exactly in line with where we took off our tactical bullish call on December 5th at 4071. The main difference is that stocks are now significantly more expensive with the [equity risk premium] at 168 basis points versus 216bps back then.”

Wilson also made an interesting point about the experience current company executives lack about today’s macroeconomic conditions. In other words, any upbeat forecasts from senior executives should be questioned:

“We would caution that this may, in fact, be a false sense of confidence as most executives have never operated in such a unique and difficult environment with respect to operating leverage. Just as CEOs were likely surprised by the upside in margins and profits in 2020-21, we think they are likely to be surprised on the downside as this operating leverage dynamic has clearly reversed.

“Based on the spread between our Leading Earnings Indicator and the consensus bottom up forecasts that are heavily based on company guidance, the risk for further surprises to the downside on earnings is nearly as significant as we have ever seen—a period that includes both the GFC and Tech bubble cycles in 2008 and 2001.”

Wilson’s team thinks consensus earnings forecasts are 10% to 20% too high!

Goldman Sachs tacked in a different direction. Goldman’s Jan Hatzius said his team’s review yielded four buoyant insights:

“First, corporate revenue trends are consistent with positive but below-potential economic growth. Second, the pullback in earnings and earnings expectations is not particularly concerning for the broader economic outlook. Third, labour shortages have eased significantly further. And fourth, wage pressures are easing but will likely linger well into 2023.”

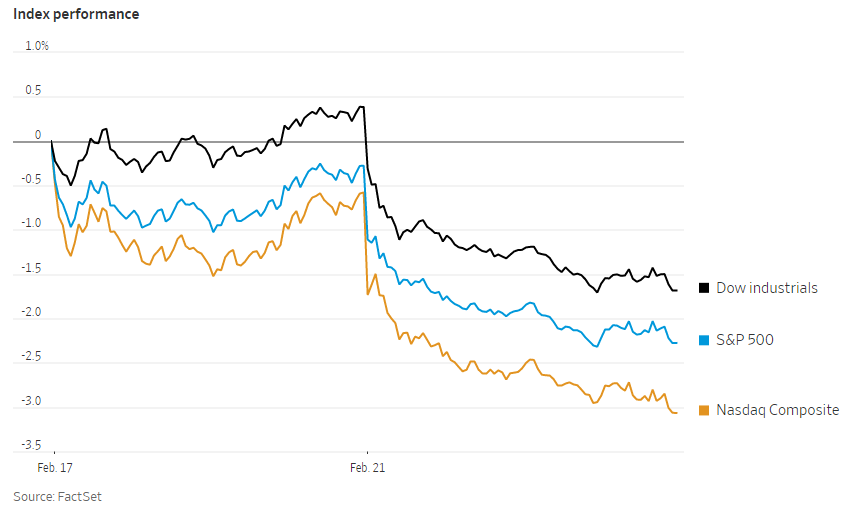

US stocks record worst day in two months

You’ve likely heard.

Wall Street had a bad day, the worst day in two months. The Dow Jones Industrial Average fell 2.1% and is now down year to date and down over the past 12 months.

Analysts had one culprit squarely in their sights — the market’s realisation that central banks will hold interest rates high for longer than initially expected (or hoped, really).

Home Depot’s disappointing sales forecast was also an accomplice in sending US stocks lower.

Source: Wall Street Journal

Good morning

Good morning.

We’ve got quite a bit to unpack today as the big decline in US stocks overnight flashes a message to markets everywhere that interest rates are likely to wreak havoc on equities for a while yet.

We also have more ASX companies reporting their results, including Rio Tinto, Flight Centre, Domino’s Pizza, Santos, WiseTech, Woolworths, and Lovisa.

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988