ASX News Live | ASX Dips; Qantas and Eagers Post Record Profit

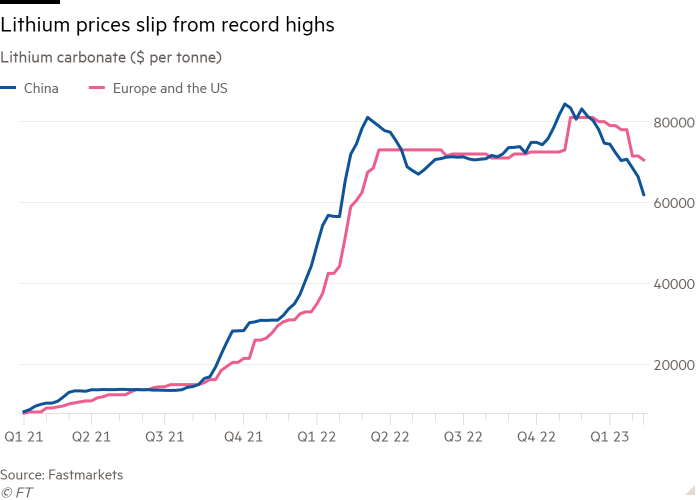

Chinese lithium prices fall 30% in past three months

Lithium prices in China fell 30% in the last three months after demand for EVs waned in the world’s largest EV market.

According to Fastmarkets, prices fell 29% from November highs to US$61,795 a tonne.

Fastmarkets lithium analyst Jordan Roberts said ‘there has been persistent weakness in China’.

Roberts argued the market is waiting to see the impact from China’s reduced EV subsidies and dipping consumer confidence.

That said, lithium prices are still elevated compared to a few years ago. Added to that, lithium prices for delivery to the US and Europe have fallen only 10% in the same period, according to data from Fastmarkets.

So is this a lull or a deep normalisation of lithium prices?

On the one hand, lithium is a key component of electric vehicles, vehicles whose sales are only set to grow from here.

On the other hand, Stein’s Law suggests things that can’t go on forever, don’t.

Source: Financial Times

What is going on with Cogstate?

Cogstate (ASX:CGS) — developer of brain health assessment technology — has entered a voluntary suspension to answer a price query from the ASX.

Cogstate was already in a trading halt since Tuesday, the day it received the price query from the exchange.

Originally, Cogstate said it would have its answer ready by today at the latest. But in announcing the voluntary suspension today, Cogstate didn’t pin down a time-frame.

How long does it take to answer a price query?

If you’re not aware of any reason at all why your company fell 30% in a matter of days, why delay the response?

Or does the lengthy time to respond suggest Cogstate is aware of reasons why its stock is down 30% since Monday on no announcements?

Humm considers pouncing on less well capitalised competitors

Despite effacing ‘BNPL’ from its business segment names, Humm is ready to pounce if ‘less well capitalised competitors cease to operate in the ANZ market’.

Laybuy is set to delist from the ASX and Openpay called in the receivers. There is expectation in the industry that Openpay’s collapse won’t be the last.

The carcasses of smaller firms like Openpay offer swooping opportunities for bigger players like Humm and even Zip, despite Zip’s own issues with liquidity.

In its 1H23 update, Humm said it sees ‘significant near-term opportunities to grow merchant and customer numbers as smaller, less well-capitalised competitors cease to operate in the ANZ market.’

Dissent in the boardroom, or what a divided Fed means for markets

It was only three weeks ago that the Fed’s tamer 25 basis point hike sent stocks flying.

The move was, to the market, a sign that an end was potentially in sight for interest rate rises.

But with the release of the meeting’s minutes overnight, that’s not looking so sure now…

What we’re starting to see is a divergence between Fed board members.

Granted, differing opinions on the pace of rate hikes or cuts are not exactly new. The whole point of the central bank is to draw a consensus from a range of options. But what clearly stood out to the market is just how divided the Fed appears to be right now.

As CNBC reports:

‘A “few” members said they wanted a half-point, or 50 basis point, increase that would show even greater resolve to get inflation down.

‘Since the meeting, regional Presidents James Bullard of St. Louis and Loretta Mester of Cleveland have said they were among the group that wanted the more aggressive move. The minutes, however did not elaborate on how many a “few” were nor which Federal Open Market Committee members wanted the half-point increase.

‘“The participants favoring a 50-basis point increase noted that a larger increase would more quickly bring the target range close to the levels they believed would achieve a sufficiently restrictive stance, taking into account their views of the risks to achieving price stability in a timely way,” the minutes said.’

Dissent in the boardroom

Now, the most interesting part of this revelation, as CNBC notes, is that we don’t know how many ‘a few’ is. It could just be one or two members erring on the side of caution, or it could be a handful of dissenters insisting on a need for bigger and quicker rate rises.

Given the outspoken remarks from Bullard and Mester, I’d wager that it’s more likely the latter. But that is pure speculation on my part.

For the market and investors like yourself, it doesn’t really matter.

The bigger problem is just how at odds the two camps are. After all, whenever Jerome Powell talks, he clearly stresses the importance of avoiding recession. These minutes, on the other hand, show that others are far more worried about getting inflation under control at any cost.

As a result, I’m worried we could wind up with the worst of both worlds. Just like this comment from a ZeroHedge article notes:

‘The biggest takeaway from the Minutes appeared to be the contradiction of Fed Chair Powell’s nonchalance at the easing of financial conditions, which is in itself a hawkish shift (despite an overall sentiment gauge suggesting this was a notably dovish minutes).’

What the Fed is saying and what it’s doing are two different things.

And this, in my view, is indicative of many of the problems facing the US economy right now.

There’s a whole lot of talking, a whole lot less doing.

https://www.moneymorning.com.au/20230223/why-the-fed-mutiny-is-a-warning-for-all-investors.html

Humm down 8% on 1H23 result: scales back BNPL operations

If you thought BNPL was a tongue-twister, how about PosPP?

Fintech Humm Group (ASX:HUM) decided to rename its BNPL business to Point of Sale Payment Plans (PosPP) to ‘more accurately reflect its products and services’. Humm, rather defensively, then added:

“The market definition of BNPL is attributed to small ticket financing which represents less than 1.2% of total receivables of the Group.”

We don’t offer BNPL services, but PosPP services. And, anyway, even if we did, they represent 1% of our receivables, so…

Humm did more than just scrap BNPL from its business segment name. It also scrapped its ‘PosPP products’ in New Zealand and paused originations to bundll ‘pending replatforming of this product’.

Bundll was its stand-alone BNPL product set to be consolidated under Humm’s official brand.

Source: bundll

Distancing itself away from the bombed out BNPL sector didn’t help Humm’s stock on Monday. HUM shares are currently down 8%. Proudly BNPL Zip is down 7%.

Blackmores’s inventories miscalculation hurts cash flows

Blackmores’s cash generated from operations in 1H23 fell 61% to $18.8 million after payments to suppliers and employees rose 11% to $357.8 million.

Inventories also grew 9% to $168.8 million in 1H23.

Since BKL also paid over $5 million in dividends, the company ended up shrinking its cash balance from $82 million to $75 million at the end of the half. That $75 million is important because ‘much of it is required to fund growth in International markets and investments in Technology and Digital.’

The steep drop in operating cash flow was also partly due to a blown inventory call as Blackmores miscalculated the durability of COVID-19 induced demand:

“The reduction in operating cash flow before interest and tax of 61.7% to $18.8 million reflects the lower EBITDA and the Group’s planned increase in inventory to ensure product availability in anticipation of a COVID-19 surge in demand which did not materialise in the half. Inventory also increased to ensure ongoing product availability for customers which helped to deliver improvements in customer service levels during the period. The Company expects inventory to reduce progressively.”

Blackmores down 8% on 1H23

Vitamins and nutritional supplements retailer Blackmores (ASX:BKL) is down over 8% after the release of its 1H23 results.

Blackmores’ 1H23 revenue fell 1.6% to $338 million yet profit rose 19.6% to $24.3 million, reflecting the higher proportion of earnings from ANZ and China versus earnings from its Indonesia JV compared to 1H22.

Revenue was up in the ANZ and China markets but was offset by a steep drop in international sales. International revenue fell 15%, with Blackmores pointing to 1H23 ‘lapping significant COVID-19 surges’ in Indonesia, Malaysia and Thailand.

As a result, underlying EBIT for the international segment fell 40% and the EBIT margin shrank to 11.8%.

Nonetheless, Blackmores materially bumped its interim dividend to 87 cents, up 38.1% on 1H22. That’s a dividend payout ratio of around 70% of statutory NPAT.

BKL thinks its balance sheet is strong enough to accommodate a dividend payout range of 40%-70% of statutory NPAT, up from 30%-60%.

Chief Executive Officer, Alastair Symington, commented:

“Blackmores delivered a solid result with continued revenue and earnings growth momentum in its Australia/New Zealand and China segments offset by its International segment which lapped a very strong prior corresponding period (pcp) that primarily included COVID-19 demand surge for immunity products. “The Company has announced a strong interim dividend of 87.0 cents per share fully franked, an increase of 38%, with an increased dividend payout range.

“While the near-term operating environment remains somewhat uncertain with continuing themes of cost inflation and rising interest rates impacting consumer sentiment and behaviour, we remain focused on executing our strategic and commercial plans and leveraging the Group’s channel and geographic diversity.”

If Blackmores’ 1H23 had a theme, it would be cost savings. ‘Cost savings’ was mentioned 14 times in the company’s half-year results announcement, with Blackmores saying it is on track for $55 million in annualized gross cost savings by the end of FY23.

The business said it also identified a further $34-44 million in gross savings over FY24-FY26.

Talga down 15% following capital raise

Battery materials junior Talga Group (ASX:TLG) is down 15% after exiting a trading halt following a capital raise.

Talga raised $40 million from an institutional placement, issuing 25.8 million new shares at $1.55 a share, a 11.5% discount to TLG’s 20-day volume weighted average price.

The newly minted 25.8 million shares accounted for 7.7% of Talga’s total ordinary shares on issues prior to the placement.

The proceeds will fund Talga’s Vittangi Anode Project in Sweden, including ‘earthworks and site infrastructure at the Luleå anode refinery site, commencement of procurement of anode equipment and detailed engineering, scaled up EVA production, silicon anode scale-up including securing commercial site, and general working capital.’

TLG is up 15% in the past 12 months.

Zip thinks it can be cash EBTDA positive by HY24

Since 2022, Zip has changed its messaging to the market. Profitability is now its focus, not growth at all costs.

Speculative growth markets have been abandoned. New business ventures scrapped. And corporate fat trimmed wherever possible.

Despite these efforts, Zip is still running up large losses, including 1H23.

But the BNPL firm thinks it can be ‘positive cash EBTDA during HY24’. That’s not too far away!

To support this target, Zip rattled off some figures:

- ‘Zip US and NZ delivered positive cash EBTDA in November and December.

- ‘Zip US and NZ remain on track to exit FY23 with positive cash EBTDA on a sustainable basis, along with Zip’s AU business which has been cash flow positive for four years.’

Co-founder and global CEO Larry Diamond reiterated the message today, stating:

“In the US, Zip delivered positive cash EBTDA in November and December with a very strong seasonal performance and remains on track to exit FY23 with positive cash EBTDA on a sustainable basis, joining the Australian business which has already been profitable for four years. The US opportunity remains in its early stages with the total addressable market estimated to be almost US$10 trillion and BNPL penetration still under 2% of total payments, demonstrating the sheer size of the opportunity that we are positioned to capture. We are also pleased to see our ‘shop anywhere’ proposition is increasingly resonating with customers who shopped at over 500k locations in the half.”

$ZIP:

– 'Zip US and NZ delivered positive cash EBTDA in November and December.

– 'Zip US and NZ remain on track to exit FY23 with positive cash EBTDA on a sustainable basis, along with Zip’s AU business which has been cash flow positive for four years.' pic.twitter.com/TLhY4DfZ1h— Fat Tail Daily (@FatTailDaily) February 22, 2023

Zip’s 1H23 revenue rises 19% but losses widen to $240 million

Struggling BNPL fintech Zip (ASX:ZIP) posted a total comprehensive loss for 1H23 of $241 million, up from $170 million in 1H22.

The loss widened despite revenue growing 19% to a record $351 million. Zip has now accumulated over $2 billion in losses.

Zip’s presentation featured the usual hits — record operating metrics that don’t translate to profit. The records this time were transaction volume of $4.9 billion, up 10% YoY, and transaction numbers of 42.2 million, up 17% YoY.

Source: Zip

The widening loss did not stop Zip from saying it ‘remains well funded with sufficient available cash and liquidity to deliver on positive group cash EBTDA during HY24’.

With its current cash burn, can it make it?

Zip’s operating cash flow was negative $226 million in 1H23, ending the half with $154 million in cash and cash equivalents and $116 million in restricted cash.

The rising interest rate environment and Zip’s higher reliance on debt instead of capital raises saw its interest payments double in 1H23 to $68 million.

The importance of household debt to the RBA’s monetary policy

Switching from the US Fed to the RBA now.

If you wondered why the Reserve Bank’s official cash rate is materially lower than most of its peers, look no further than our household debt.

In a very interesting admission, the RBA said Australia’s high level of debt makes the monetary policy pass-through much more effective, meaning it can do more with less:

“Members also noted that the cash rate was lower than policy rates in many other comparable economies. While wages growth remained lower here than elsewhere, Australia’s positive exposure to higher commodity prices and the extra savings buffers accumulated by households were estimated to be larger than in other countries. There were also notable differences in fiscal policy and population growth around the globe. Members observed that the cash-flow channel of monetary policy was stronger in Australia than in other countries, given the high level of variable-rate debt.”

Additionally, the central bank now thinks the rising interest rates on variable-rate home loans and the consequent mortgage payments are ‘projected to reach their highest level on record (as a share of household disposable income).‘

The key passage from the latest Fed FOMC meeting minutes

The US Fed still envisages more interest rate hikes. That’s the big takeaway from the latest Fed FOMC meeting minutes.

The key passage is here:

“In discussing the policy outlook, with inflation still well above the Committee’s 2 percent goal and the labor market remaining very tight, all participants continued to anticipate that ongoing increases in the target range for the federal funds rate would be appropriate to achieve the Committee’s objectives. Participants affirmed their strong commitment to returning inflation to the Committee’s 2 percent objective. In determining the extent of future increases in the target range, participants judged that it would be appropriate to take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments. Participants observed that a restrictive policy stance would need to be maintained until the incoming data provided confidence that inflation was on a sustained downward path to 2 percent, which was likely to take some time.”

So all Fed officials see more interest rate hikes ahead.

And all agree that a restrictive policy must remain in place for a while yet. After all, recent economic data does not scream ‘inflation is on a sustained downward path to 2%’ just yet.

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988