ASX News LIVE | ASX Opens Down; Iron Ore Slumps Below US$100; AirTrunk $20b Sale Nears Deadline

Market close update

The ASX 200 closed near flat, falling -0.08% ti 8,103.2 on a relatively quiet day on the markets as Wall St remained closed for Labor Day.

An overnight -3.9% drop in Iron ore Futures was today’s major market mover.

This pushed major miners to close lower, with BHP down 1.74%, Fortescue falling 2.64%, and Rio Tinto down 1.66%.

Those losses were slightly balanced out by gains from the Big Four, with all banks reversing morning losses to close higher.

Commonwealth Bank pushed to a new all-time high for the second consecutive session, with an intraday peak of $143.305.

Consumer staples also had a tough day of selloff, with Woolworths falling -2.8%, and Coles closing down -2.4% to $18.50.

Lovisa was the major benchmark top gainer today, up by +4.28%, seeing its stock recover slightly from its recent -21% drop despite profit growth.

Tomorrow, we have GDP figures as the likely major news for the day, so we’ll cover all of that here tomorrow!

Fonterra Invests $138m in New Cream Facility

New Zealand’s dairy giant Fonterra [ASX:FSF] has announced plans to construct a NZ$150 million Ultra-High Temperature (UHT) cream production plant at its Edendale location.

This move aims to satisfy the increasing appetite for laksa and milk products in Asian markets.

During a trip to Malaysia, Fonterra CEO Miles Hurrell said:

“The UHT cream market is experiencing robust growth. Our projections indicate a global demand increase exceeding 4% annually from 2023 to 2032.”

The new facility will initially be able to process over 50 million litres of UHT cream, with potential expansion to surpass 100 million litres by 2030.

Fonterra shares are up slightly in trading today, at $4.15 per share.

Over the past 12 months, the diary large cap has gained 43%, putting it as one of the top performers in its sector.

Australia’s Trade Imbalance Surges to $10.7 Billion

Australia’s current account deficit expanded to $10.7 billion in the second quarter of this year, marking the largest gap in six years. This significant increase was primarily driven by declining commodity prices and increased overseas payments.

The latest figures far exceeded analysts’ projections of a $5.9 billion shortfall. Additionally, the first quarter’s deficit was revised upward to $6.3 billion from the initially reported $4.9 billion.

Tom Lay, head of international statistics at the Australian Bureau of Statistics (ABS), noted today:

‘We observed a second consecutive quarterly decline in iron ore and coal prices, resulting in goods export prices dropping 5.4% compared to the same period last year.’

The ABS reported that net exports would contribute 0.2% to the second quarter’s Gross Domestic Product (GDP), falling short of economists’ expectations of a 0.6% boost.

Australia’s terms of trade (a measure of export prices relative to import prices) decreased by 3% from the previous quarter and showed a 3.8% decline over the 12 months ending in June.

These numbers are likey going to feed into a soft GDP figure that is expected tomorrow. Treasurer Jim Chalmers has already warned of ‘subdued growth‘.

Latest Fat Tail Daily Video

Here’s the latest from the new Fat Tail Daily video series.

Publisher James ‘Woody’ Woodburn will be sitting down with our Fat Tail Daily editors to discuss the key trends and offer unique insights into market movements.

If you have any thoughts about the length, format, or topics you would like discussed, send us an email at support@fattail.com.au with the subject header: ‘Fat Tail Daily Video Feedback’.

Thanks, and enjoy today’s discussion with Australian Gold Report Editor Brian Chu.

Midday market update

The ASX 200 is flat around midday, with the major benchmark climbing from its morning losses to sit at 8,108.1 nearing lunch.

Six of the eleven sectors are up today with Tech leading up +0.45%, while Staples -1.87% is the worst performing sector, with Woolworths down by -3.29% and Coles down by -2.16%.

Its a fairly quiet day of trading with lower average volumes as US markets remain closed for Labor Day and many local traders awaiting GDP figures which will be released tomorrow.

The biggest market moves on the ASX 200 so far today are Contact Energy, up 5.11%, and Stanmore Resources, down by -3.43%.

The major banks hover between +0.2-0.5% this morning, while the major miners are all down on the back of falling Iron ore Futures, which plunged nearly 4% overnight.

Australia’s current account figures were released this morning. They show that the deficit expanded to $10.7 billion in the June quarter, marking the largest shortfall in six years. We’ll explore that more next.

The ABS reported that net exports would contribute 0.2 percentage points to the June quarter’s gross domestic product (GDP).

So far, Treasurer Jim Chalmers has already given a pre-warning that we should expect ‘soft and subdued’ GDP growth as interest rates continue ‘smashing the economy,‘ as he put it.

Major miners pull the ASX down

An overnight 3.9% slump in Iron ore Futures on the Singapore exchange has brought down the ASX 200 in morning trading.

ASX 200 futures pointed to a positive day, and so far, it looks like the major benchmark is trying to climb out of this morning’s drop, but major miners are holding it back.

So far, we’ve seen:

BHP is down -0.38% to $40.18 per share.

Rio Tinto is down -0.35% to $109.56 per share.

Fortescue is down -0.14% to $18.16 per share.

The moves come as concerns about Chinese manufacturing and property are once again in vouge.

Despite the worries, the latest data from Caixin’s China manufacturing PMI for August showed modest growth. Figures came in at 50.4, that is up 0.6pts from the sub-50 reading last month, which denotes contraction.

However some troubling signs are emerging within Inventories, which are starting to grow. Stockpiling is being seen in coal, oil, and iron ore.

Source: Bloomberg

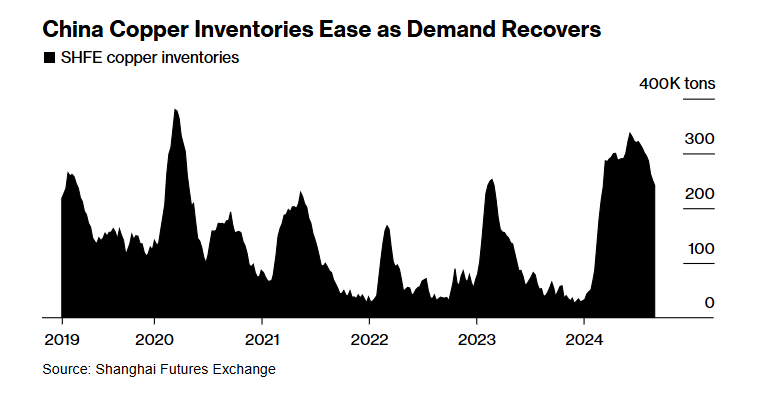

One bright spark is copper, which has seen its inventories ease as demand from renewables and other advanced manufacturing take the place of older manufacturing hubs in China.

The major use in the first wave of this copper demand was Chinese solar panels. However, that market has been in the midst of a tough winter, with what was described as a ‘bloodbath’ of an earnings season.

Signs are that things are beginning to normalise there also.

Source: Bloomberg

Consumer confidence begins to climb out of its hole

The latest ANZ-Roy Morgan Consumer Confidence Index shows things are starting to move in the right direction in the eyes of Australians.

The latest figures showed a 0.5pts increase as expectations of inflation eased to 4.6%, their lowest since late 2021.

Meanwhile, households are feeling more secure about their finances, with the survey finding confidence in future financials at a five-month high.

With things starting to look positive again, what will be the next major decision by the RBA to boost consumers’ feeling that mortgages will ease soon?

ANZ-Roy Morgan Consumer Confidence rose 0.5pts. Inflation expectations eased to 4.6%, its lowest point since late 2021. Household confidence in the future financial situation rose to a 5mth high, back into positive territory. #ausecon @madelinedunk @cfbirch @RoyMorganAus pic.twitter.com/GxUBtl2gYS

— ANZ_Research (@ANZ_Research) September 2, 2024

EML Payments Divests Sentenial to GoCardless for $53.4 Million

Morning Market Update

Good morning. Charlie here.

The ASX 200 opened down -0.33% to 8,083.1 as major miners sold off on early trading as Iron ore futures fell -3.9% overnight.

Iron ore prices had been making a slow comeback, almost recovering 10% in the past two weeks, but the latest tranche of data once again raises the spectre of a weakened China.

Factory activity in China contracted for the fourth straight month in August, while the latest property sales show the value of new homes fell around 26.8% from a year earlier.

That’s a steeper drop than the 19.7% decline seen in July. The accelerating fall shows that the stimulus package in May was not enough to restore confidence in the ailing sector.

US markets are taking a break for Labor Day, while European stocks finished mixed overnight as Euro manufacturing PMI also remained in contraction for August, pushing back hopes of an earlier recovery there.

On the ASX, we will keep an eye out for the major miners and cover the story of AirTrunk’s massive $20 billion sale. Plus news of EML selling Sentenial for $53 million; stay tuned.

| Name | Value | % Chg | |

|---|---|---|---|

| Major Indices | |||

| S&P 500 | 5,648 | – |

| Dow Jones | 41,563 | – |

| NASDAQ Comp | 17,713 | – |

| Russell 2000 | 2,217 | – |

| Country Indices | |||

| UK | 8,363 | -0.15% |

| Germany | 18,930 | +0.13% |

| Euro | 4,973 | +0.30% |

| Japan | 38,811 | +0.31% |

| Hong Kong | 17,691 | +1.65% |

| Name | Value | % Chg | |

|---|---|---|---|

| Commodities (USD) | |||

| Gold | 2,497 | -0.22% | |

| Silver | 28.52 | -1.22% | |

| Iron Ore | 97.25 | +0.45% | |

| Copper | 4.1217 | +3.22% | |

| WTI Oil | 73.94 | -0.16% | |

| Currency | |||

| AUD/USD | 67.87¢ | +0.30% | |

| Cryptocurrency | |||

| Bitcoin (USD) | 59,125 | +2.91% | |

| Ethereum (USD) | 2,533 | +4.11% | |

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988