ASX LIVE | ASX to Rise following Wall Street Rally, Earnings Season continues for Big Tech and XJO

Have a good evening

That’s all from me today investors.

I’ll leave you with today’s AI-generated image of today’s big news of the Twitter rebranding to X.

Silly move or a stepping stone to rebranding the image?

Only time will tell.

Cost of tariffs for Australia

The latest government research has found that China’s punitive trade war with Australia failed.

Australia’s economy suffered limited damage from trade actions by China.

The overall impact of China’s measures was a reduction of just 0.009% in GDP, once new buyers for the sanctioned products were found.

Australia’s exports had been resilient in the face of the trade actions, with barley and coal, in particular, rapidly finding new markets.

However, the authors recognized that while the economy may have been little affected, individual businesses ‘paid a heavy price.’

The research comes as Australia and China attempt to improve diplomatic relations while navigating trade disruptions, political disagreements and security concerns.

Since the election of Labor in May, high-level ministerial meetings have resumed between Australia and China.

In April, the Chinese government announced it would hold a review into its tariffs on Australian barley, in return for which Canberra suspended its case against Beijing in the World Trade Organization.

However, the review has been pushed back from China, and there have been no public announcements on similar moves on wine.

Will we see history repeat again, and China miss another trading opportunity?

Australia’s economy suffered limited damage from punitive trade actions by China, government research found, as Canberra and Beijing try to negotiate an end to tariffs on Australian barley and wine exports https://t.co/vdNaHPMFN1

— Bloomberg Economics (@economics) July 25, 2023

Market close update

ASX 200 closed up 0.46% at 7,339.7 brought higher by positive trading in the Materials and Energy Sectors — buoyed by rising commodity prices.

US equities and promises of modest Chinese stimulus also lifted global sentiment about the possibility of avoiding a hard recession.

- $AUD up +0.64% at 67.73 US cents

- ASX futures down -0.12% to 7,291.5

- S&P 500 up +0.40%

- NASDAQ up +0.19%

- DOW up +0.52%

- FTSE up +0.19%

- STOXX down -0.071%

- SSE up +2.11%

- Bitcoin down -2.15% to $US 29,139.89

- Spot gold up +0.35% to $US 1,961.40

- Iron ore up +0.04% to $US 112.51

- Brent Crude up +0.25% to $US 82.94pb

ASX 200 Sector Top Performance:

- Materials up 2.81%

- Energy +0.92%

- Telecomunication up +0.45%

The best ASX 200 individual performers:

- Champion Iron [ASX:CIA], up 5.31%

- Pilbara Minerals [ASX:PLS], up 5.23%

- Chalice Mining [ASX:CHN], up 5.18%

- Sandfire Resources [ASX:SFR], up 4.69%

- Fortescue Metals [ASX:FMG], up 4.24%

The worst ASX 200 performers:

- Domino’s PIZZA Enterprises [ASX:DMP], down 5.06%

- Credit Corp Group [ASX:CCP], down 4.42%

- Nufarm [ASX:NUF], down 3.60%

- The Star Entertainment Group [ASX:SGR], down 2.55%

- Ingenia Communities Group [ASX:INA], down 2.43%

All figures shown are from 4:18pm AEST

Opportune trade coming soon

With the all-important Australian CPI data out tomorrow midday, we can finally see if we are past peak inflation.

Current forecasts are around 5.4% (YoY), down from 5.6%.

But what does that signal?

If we aren’t surprised by something out of left field, the data should point to the RBA, and other central banks will be nearing the end of the interest rate hike cycle.

While there is some time for previous hikes to be felt, the shift in monetary policy opens up opportunities that don’t come along often.

If you’re a savvy trader, then you don’t want to miss these opportunities.

But that’s not the only big-timing trade you can make.

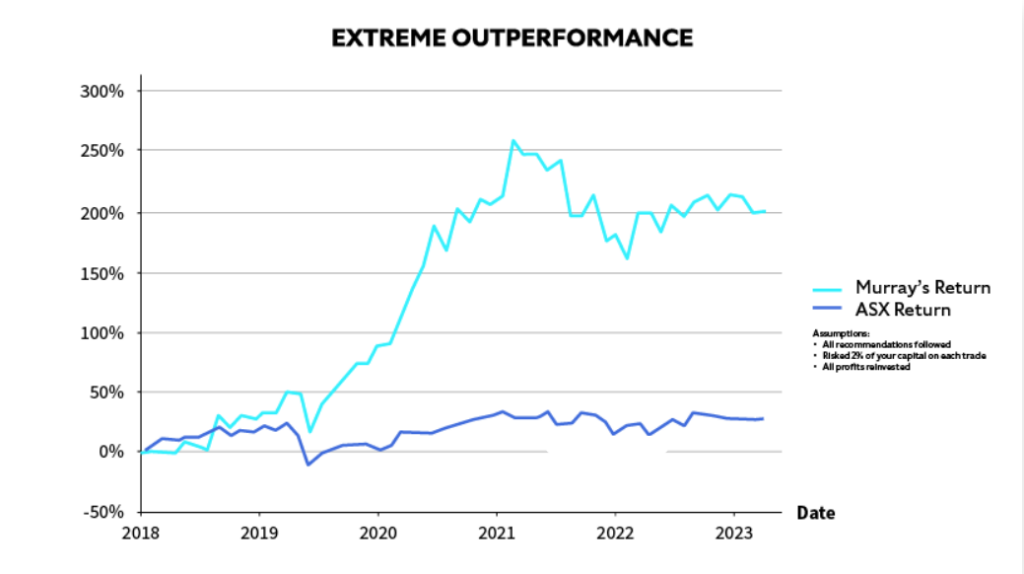

Our veteran investing expert Murray has been in a defensive position this year, waiting for a big opportunity to strike — and now he’s found it.

His track record can speak for itself.

While past performance does not guarantee a future profit, we think he might be onto something.

This will be his most significant move in the market since predicting the 2021 peak.

Want to learn more? Click here to learn how to join us for one of the smartest trades you could make this year.

Fixed income analysts split over recession chances

Flip a coin— that’s what some market analysts are saying about the outlook of the US economy.

The debate rages on between bearish textbook economists and traders who remain optimistic that the markets will experience a soft landing and continue to perform well, driven by strong earnings and a robust job market.

Fear and greed indexes have US markets at ‘extreme greed’— levels not seen since April 2021.

So who’s right?

The bond market's traditional warning that a recession is near — an inversion of the yield curve — keeps getting louder, despite increasing optimism elsewhere.

Traders have a new theory https://t.co/uAAUab4zJV

— Bloomberg Markets (@markets) July 25, 2023

AUD reverses higher as market sentiment improves

The Australian Dollar rose against the US Dollar today, after sentiment turned positive, supporting commodity currencies such as the Aussie more than safe havens like the Buck.

The AUD/USD pair traded in the 0.67s during the US session overnight.

The Australian Dollar edged higher on the back of positive market sentiment, which fostered a risk-on mood conducive to the Aussie dollar.

AUD is expected to face headwinds as inflation is predicted to fall, reducing pressure on the RBA to raise interest rates to bring inflation under control.

The Federal Reserve’s interest rate decision at 18:00 GMT on Wednesday could also impact the AUD/USD pair.

There also exists a high risk that the RBA will have to cut rates from their current 4.1% level next year if inflation continues to fall at its current rate.

This would be to provide some relief for the variable-rate mortgages, which are hurting homeowners and spending.

In the near future, the AUD/USD pair will continue to experience instability, as all these factors press on the valuations.

Mixed signals from US markets

The stock market began 2023 on a solid note, with the S&P 500 surging 27% from its bottom, emerging from its longest bear market since the 1940s.

Positive economic indicators, such as cooled inflation, a robust job market, and retail spending, have contributed to the market’s optimism, with economists raising GDP estimates for the upcoming quarters.

Despite these positive signs, there are reasons for caution. The Conference Board’s leading economic index has continuously declined for 15 months, signalling a potential economic slowdown.

Additionally, the bond market is raising concerns, with longer-term U.S. Treasury yields lower than shorter-term ones, indicating possible rate cuts by the Federal Reserve.

The stock market’s rally has puzzled some experts, given these warning signs and the rich valuations relative to history.

The S&P 500’s price-to-projected-earnings ratio is at its highest level in years, making it more vulnerable to a pullback.

While inflation has cooled, it remains above the Fed’s target. Central bank officials may consider lifting rates again, which could have unpredictable consequences for the economy and the markets.

Investors are split between optimism and caution, with some firms selling U.S. stocks to protect against a potential downturn.

The market’s resilience and future trajectory remain uncertain, leaving investors on watch for any shifts in the Federal Reserve’s stance on interest rates.

See the link below if you want to see more of our thoughts on where this leaves your trades.

https://www.moneymorning.com.au/20230724/nailing-the-goldilocks-trade.html

Victoria takes bulk of new construction projects

It seems Victoria has come out swinging in the past few months, taking the majority of major new construction projects.

The total of new projects is down 13.7% in the past year, but major cities continue to see apartments and commercial buildings greenlit as big cities still face high rent prices.

Median unit rents for June 2023 sit at:

- Sydney $670, up 27.6% this year

- Melbourne $500 up 22% this year

- Brisbane $530 up 17.8% this year

- Adelaide $430 up 13.2% this year

- Perth $480 up 20% this year

Corelogic Cordell Construction Report.

Vic taking the lion's share of new projects..

– Total number of new projects identified over the past 3 mths is 9.4% higher than the previous 3 mths.

– Total number of new projects identified over the past yr is -13.7% lower than the 12… pic.twitter.com/zinIYNXGk0

— Catherine Cashmore (@CC_CASHMORE) July 25, 2023

Midday Update

ASX 200 remains up 0.28% at 7,326.8 with little movement since the mornings jump.

Materials and Energy Sectors are the main two sectors holding the ASX up, with eight of the eleven sectors down this morning.

This is thanks to rising commodity prices, as crude oil sits above the 52-week moving average.

Here are today’s biggest gainers and losers:

ASX miners rebound

The mining sector is recovering from a sell-off with strength today as Iron ore prices edged up to US$ 112.47 a tonne.

August futures contracts on the Singapore exchange hit a high of $115.22 overnight before coming back down to $112.63.

BHP, Fortescue Metals and Rio Tinto are all up today, as well as large energy companies who are tracking with high oil prices.

Brent Crude Oil prices are up 3.27% this past 7 days, trading at US$82.79 per barrel.

China’s leaders signal limited help to economy

The important Politburo meeting has come and gone without any promises of the large stimulus package some were hoping for to restart the struggling Chinese economy.

But there was some good news for the markets.

China’s top leaders pledged more support for the struggling real estate sector and aim to boost consumption while resolving local government debt.

The ruling Communist Party’s Politburo, led by President Xi Jinping, promised ‘counter-cyclical’ policies, indicating further economic support and adjustments to property sector restrictions.

Without the larger boost, it seems that this will have a limited impact on global markets unless China can restart its growth with these small steps.

ASX movement today

ASIC accuses Vanguard of greenwashing

The Australian Securities and Investments Commission (ASIC) has accused fund management giant Vanguard of misleading investors in its over $1 billion ethical bond fund about the sustainability of its assets.

The regulator alleges that Vanguard did not screen out investments in fossil fuels as promised, and is seeking penalties and declarations of wrongdoing.

This is the second major greenwashing case brought by ASIC this year.

Good morning

ASX opens up 0.31% at 7,328.9; this follows rallies seen in the US equities markets. Optimism there is running at highs not seen since April 2021 as the bull market continues.

Meanwhile, in commodities Oil and Gas prices are up today. European gas prices are up 20% after maintenance in major plants in Norway was extended, signalling Europe’s continued sensitivity to supply issues.

- $AUD up +0.18% at 67.35 US cents

- ASX futures down -0.12% to 7,291.5

- S&P 500 up +0.40%

- NASDAQ up +0.19%

- DOW up +0.52%

- FTSE up +0.19%

- STOXX down -0.071%

- SSE down -0.11%

- Bitcoin down -3.01% to $US 29,161.63

- Spot gold down -0.34% to $US 1,954.70

- Iron ore up +0.04% to $US 112.47

- Brent Crude up +2.07% to $US 82.75pb

All figures shown are from 10:10am AEST

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988